,

5 tweets,

3 min read

Read on Twitter

1/5

The 'no deal' tariffs set to zero lines covering 87% of imports by value. Some portion of that (I don't have the by value numbers but 26% of tariff lines) was already 0%.

However, many of the imports on current non-zero lines already come in on 0% due to several reasons.

The 'no deal' tariffs set to zero lines covering 87% of imports by value. Some portion of that (I don't have the by value numbers but 26% of tariff lines) was already 0%.

However, many of the imports on current non-zero lines already come in on 0% due to several reasons.

2/5

Those reasons being ...

1. Imports from the EU

2. From FTA partners at 0%

3. From developing countries at 0%

4. Under a tariff-rate quota at 0%

5 On a 0% tariff rating anyway - not relevant as we're talking about non-zero tariff lines.

Those reasons being ...

1. Imports from the EU

2. From FTA partners at 0%

3. From developing countries at 0%

4. Under a tariff-rate quota at 0%

5 On a 0% tariff rating anyway - not relevant as we're talking about non-zero tariff lines.

3/5

This results in the current situation where 87.2% of goods by value enter the EU on a 0% tariff.

Some goods currently covered by that 87.2% will now be subject to the 13% of full remaining MFN tariffs announced in March. Therefore the potential saving here is insubstantial.

This results in the current situation where 87.2% of goods by value enter the EU on a 0% tariff.

Some goods currently covered by that 87.2% will now be subject to the 13% of full remaining MFN tariffs announced in March. Therefore the potential saving here is insubstantial.

4/5

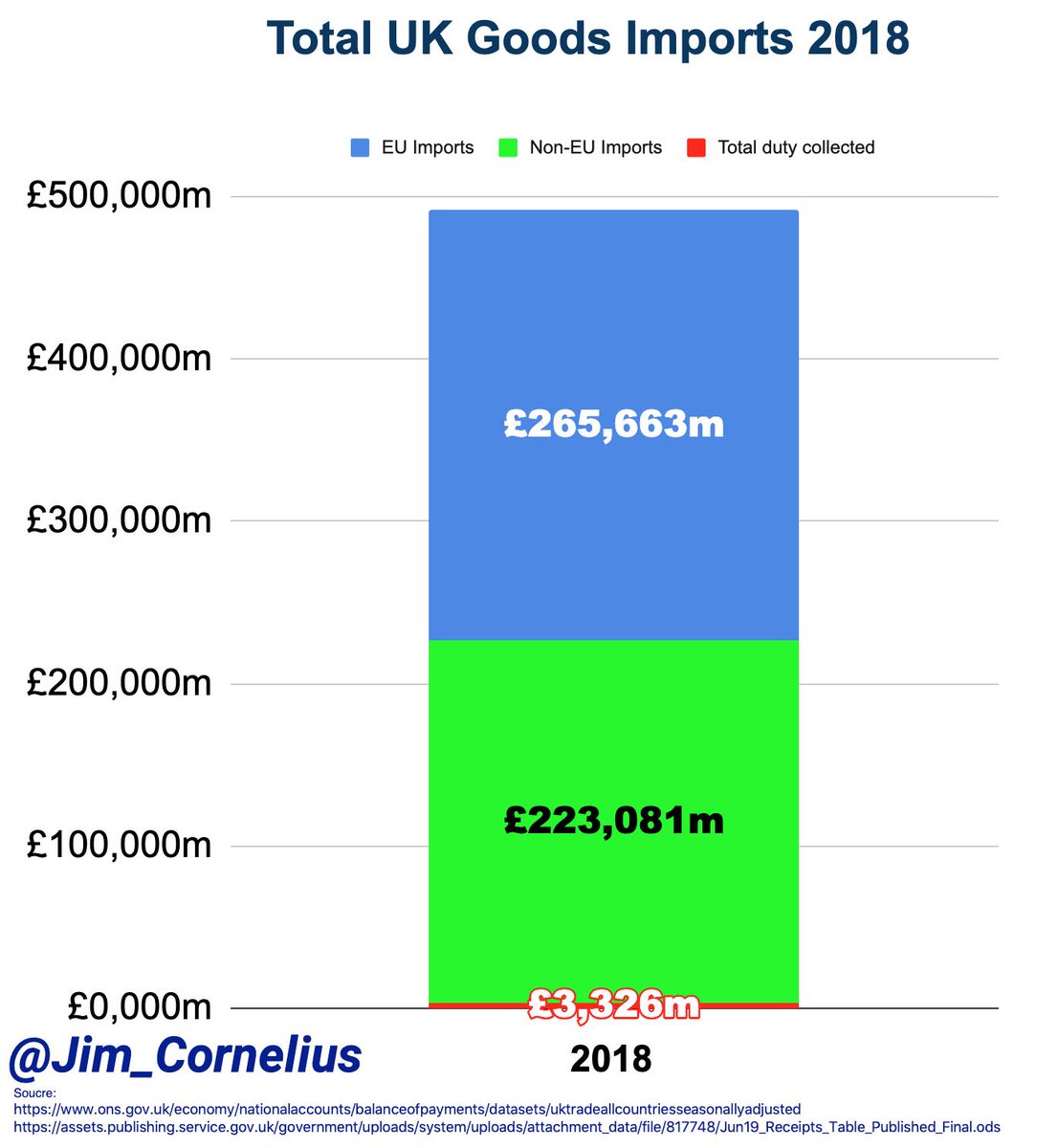

Total Imports in 2018 were £488,744m.

Total customs duties in 2018 were £3,326m

So average tariff of 0.68% on total trade

In 2018 Non-EU imports were £223,081m.

So average tariff of 1.49%. on non-EU trade.

ons.gov.uk/economy/nation…

assets.publishing.service.gov.uk/government/upl…

Total Imports in 2018 were £488,744m.

Total customs duties in 2018 were £3,326m

So average tariff of 0.68% on total trade

In 2018 Non-EU imports were £223,081m.

So average tariff of 1.49%. on non-EU trade.

ons.gov.uk/economy/nation…

assets.publishing.service.gov.uk/government/upl…

5/5

With most existing trade partners, significant savings are illusory.

Hope rests on finding cheaper (despite pound falling) alternate sources in quantity, previously tariffed out of the market, to replace current EU and trade partner sources.

But where are these in reality?

With most existing trade partners, significant savings are illusory.

Hope rests on finding cheaper (despite pound falling) alternate sources in quantity, previously tariffed out of the market, to replace current EU and trade partner sources.

But where are these in reality?