,

16 tweets,

9 min read

Read on Twitter

MILLENNIALS

You might think “avocado toast” or “participation trophies.” But they’re about to become the biggest adult cohort in America, and Wall Street wants to know if they can lead the U.S. economy (and stock market) to greater heights.

Thread!

bloomberg.com/graphics/2019-…

You might think “avocado toast” or “participation trophies.” But they’re about to become the biggest adult cohort in America, and Wall Street wants to know if they can lead the U.S. economy (and stock market) to greater heights.

Thread!

bloomberg.com/graphics/2019-…

I worked with the masterful @hecharts to make graphics that provide a better sense of where millennials are at right now.

Using Fed data and other statistics, we can see how young Americans (under 35) now compare to those of the past. And how they compare to older generations.

Using Fed data and other statistics, we can see how young Americans (under 35) now compare to those of the past. And how they compare to older generations.

@hecharts Some good news: Millennials are starting to make more money.

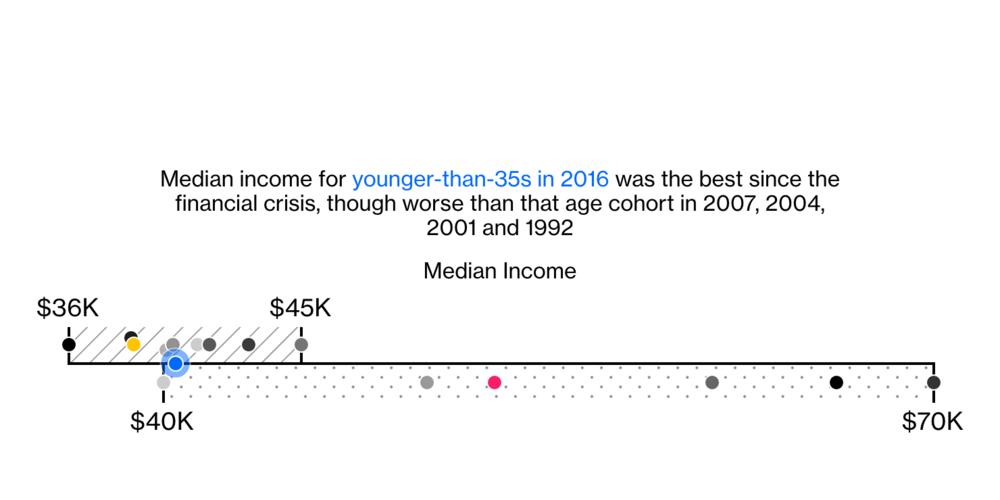

The unemployment rate has declined and wage growth has somewhat picked up in recent years. So median income is finally bouncing back after a big drop in the wake of the Great Recession.

The unemployment rate has declined and wage growth has somewhat picked up in recent years. So median income is finally bouncing back after a big drop in the wake of the Great Recession.

@hecharts The following is also good news -- and somewhat surprising.

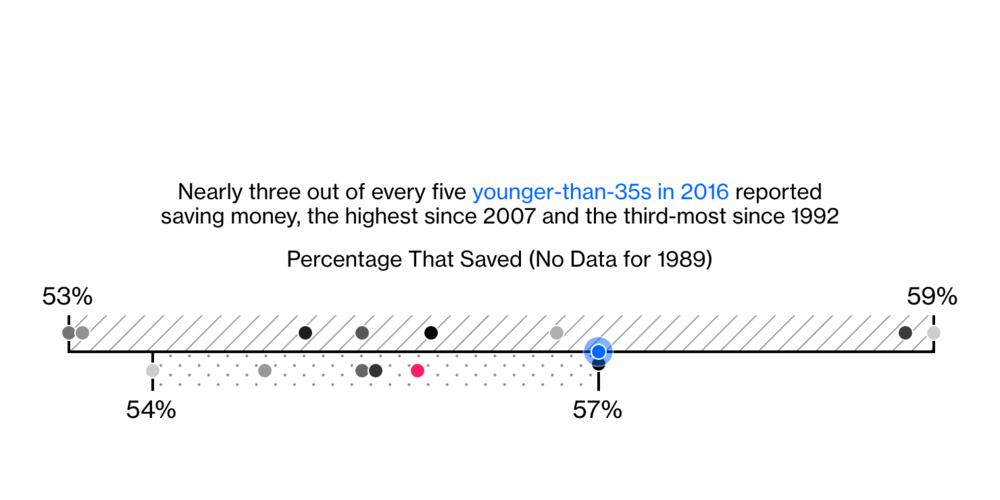

57% of millennials report saving money. That’s the most for the youngest cohort since 2007. They’re right there with 35-44 year olds, who had the advantage of entering the job market before the financial crisis.

57% of millennials report saving money. That’s the most for the youngest cohort since 2007. They’re right there with 35-44 year olds, who had the advantage of entering the job market before the financial crisis.

@hecharts And yet, here’s one of the core issues with the “Millennial Balance Sheet.”

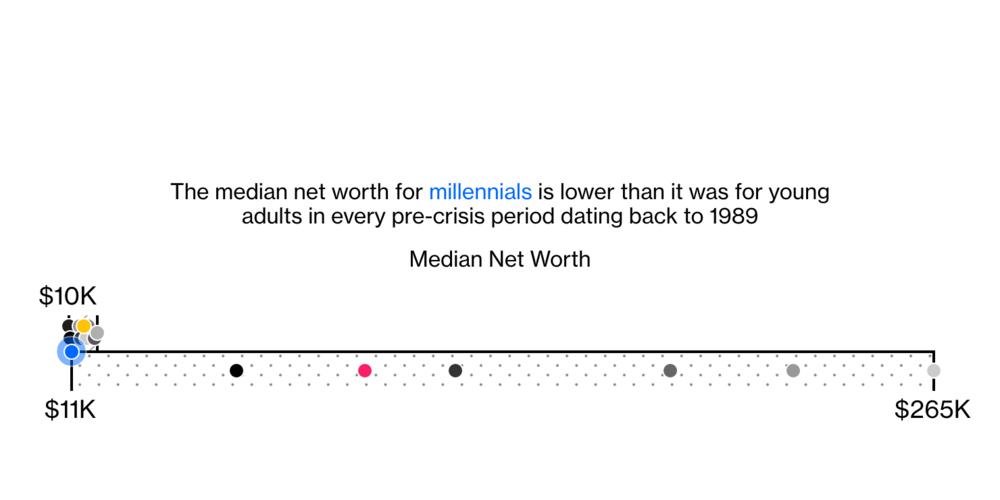

Adjusted for inflation, their median net worth of $11,000 is lower than it was for young adults in every pre-crisis period dating back to 1989.

We’ll break down what’s holding them back.

Adjusted for inflation, their median net worth of $11,000 is lower than it was for young adults in every pre-crisis period dating back to 1989.

We’ll break down what’s holding them back.

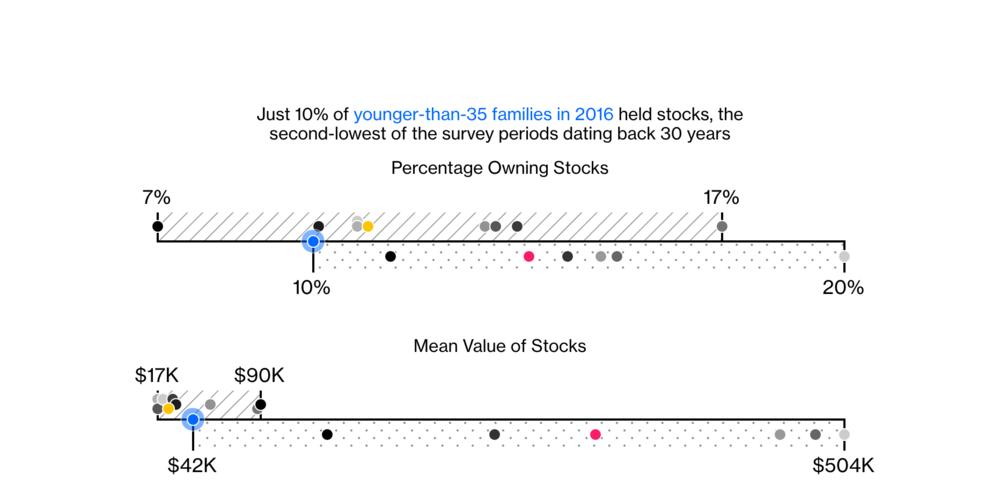

@hecharts Millennials’ investing habits are fascinating.

At first glance, it looks like they’re shunning the stock market like few younger generations before them.

At first glance, it looks like they’re shunning the stock market like few younger generations before them.

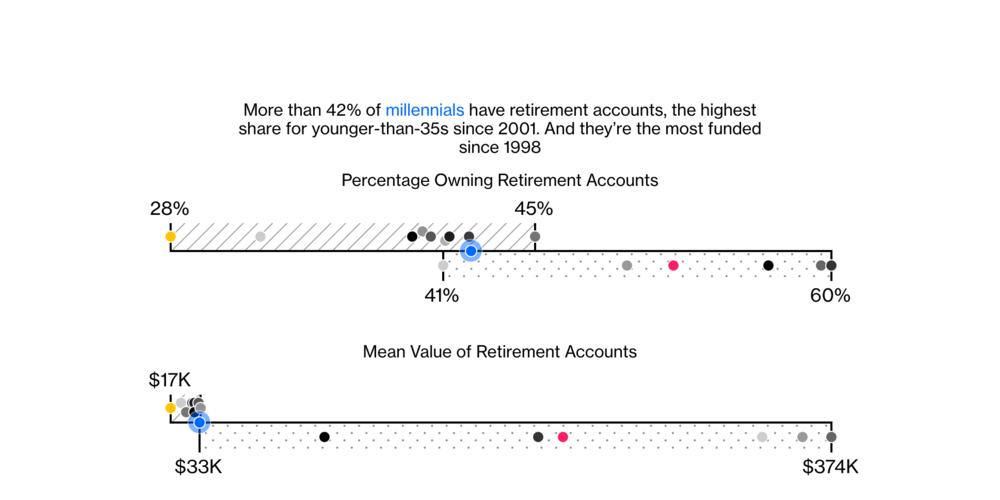

@hecharts But! That number might be selling millennials short.

More young people own retirement accounts than any time since 2001. And they’re the most well-funded since 1998.

Also, Fidelity found that 69% of millennials are all-in on target date funds, which are loaded up with stocks.

More young people own retirement accounts than any time since 2001. And they’re the most well-funded since 1998.

Also, Fidelity found that 69% of millennials are all-in on target date funds, which are loaded up with stocks.

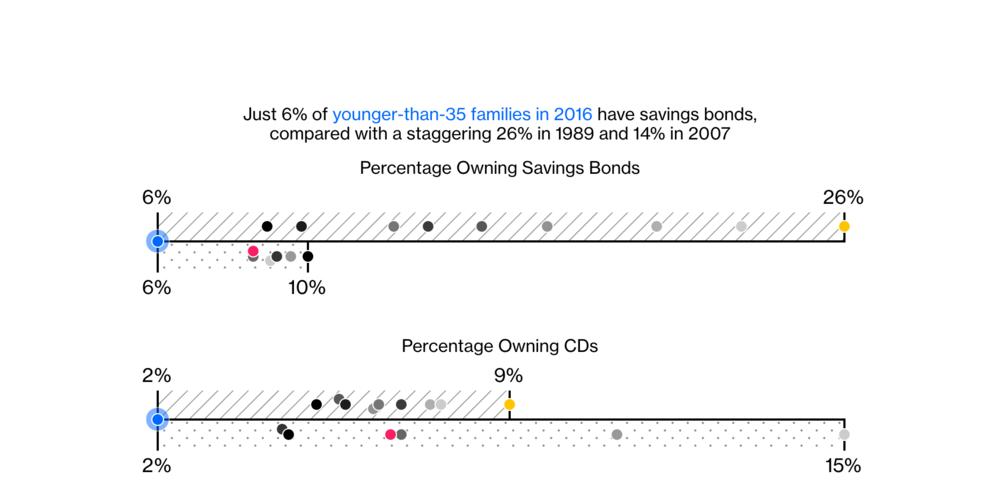

@hecharts This is fairly obvious but I’m a fixed-income guy and had to include it.

Millennials don’t do savings bonds or CDs. And if interest rates stay as low as they are now, they possibly never will.

Millennials don’t do savings bonds or CDs. And if interest rates stay as low as they are now, they possibly never will.

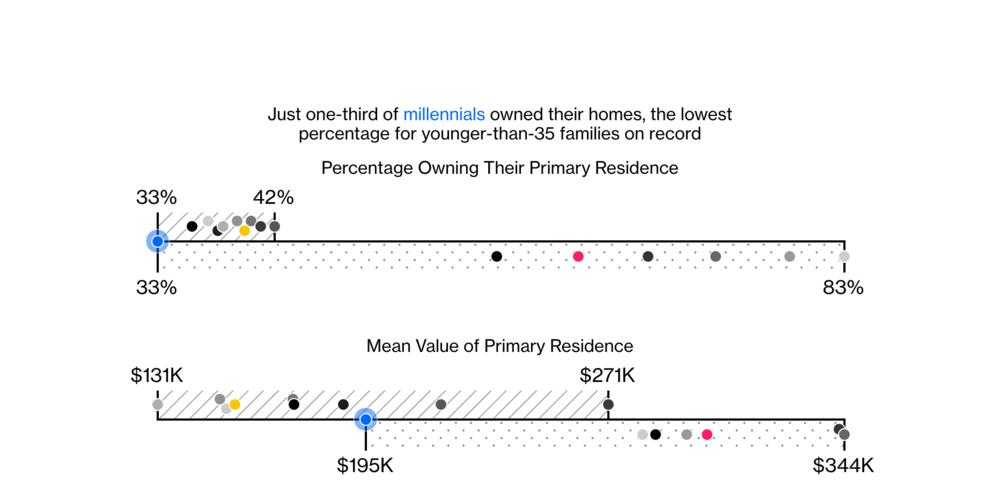

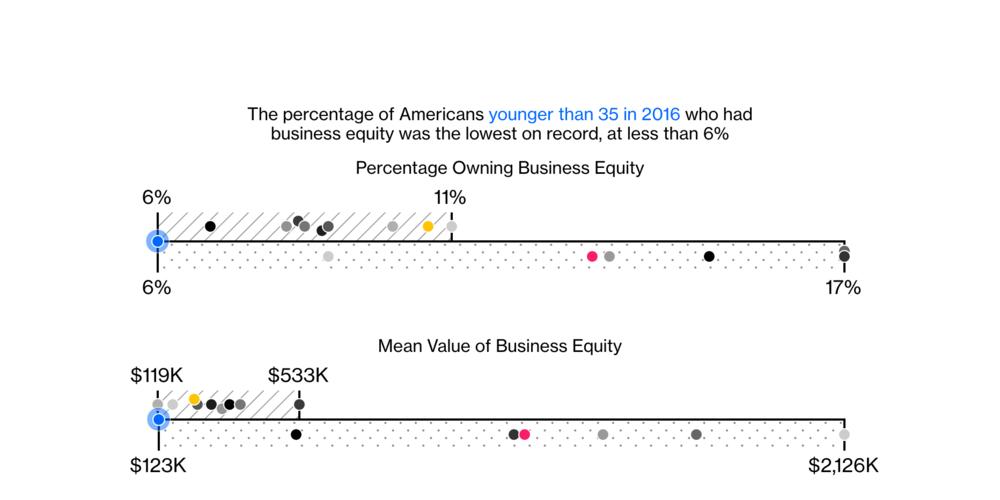

@hecharts Millennials are breaking records. But not necessarily in a good way.

Never before have so few families under age 35 owned their primary residences. The same goes for business ownership.

Never before have so few families under age 35 owned their primary residences. The same goes for business ownership.

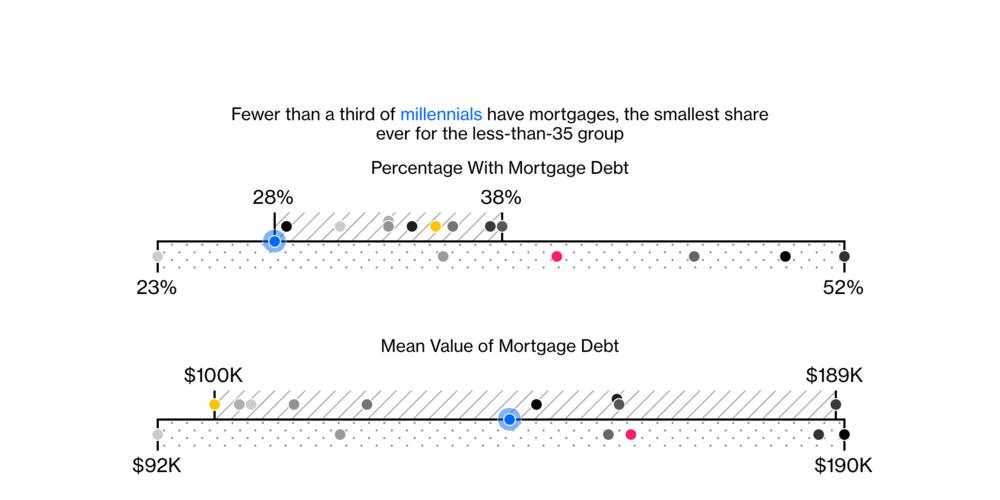

@hecharts Along those same lines, fewer young Americans have mortgage debt than ever before.

That’s a BIG item on the liabilities side of the balance sheet that’s missing among millennials.

That’s a BIG item on the liabilities side of the balance sheet that’s missing among millennials.

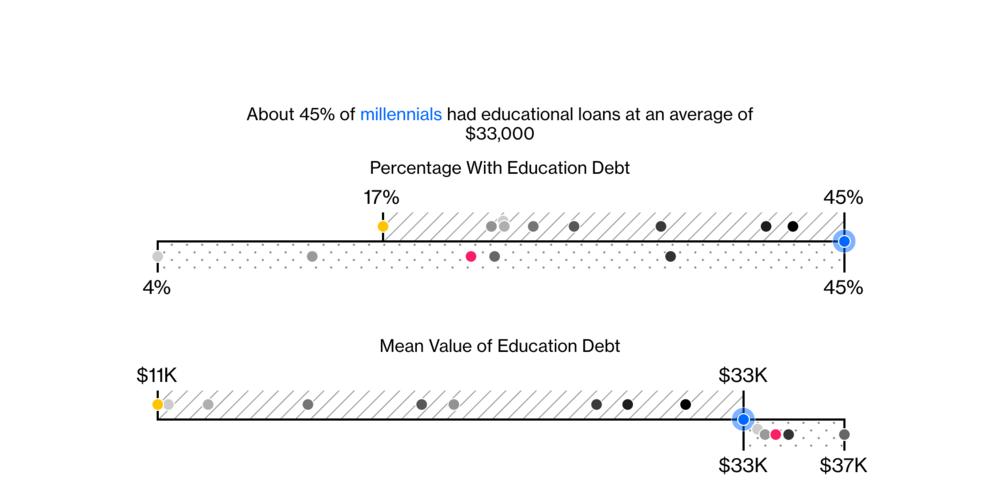

@hecharts But you probably know where I’m going next: Student loans.

They are an ever-larger burden for millennials. 45% of people under-35 had education debt, with an average value of $33,000. Both of those are record highs.

That’s a tough starting point for accumulating wealth.

They are an ever-larger burden for millennials. 45% of people under-35 had education debt, with an average value of $33,000. Both of those are record highs.

That’s a tough starting point for accumulating wealth.

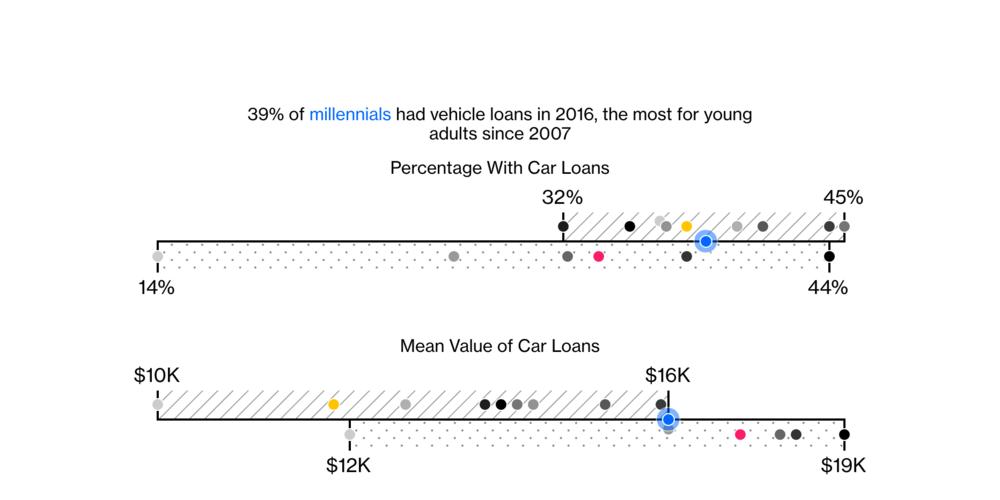

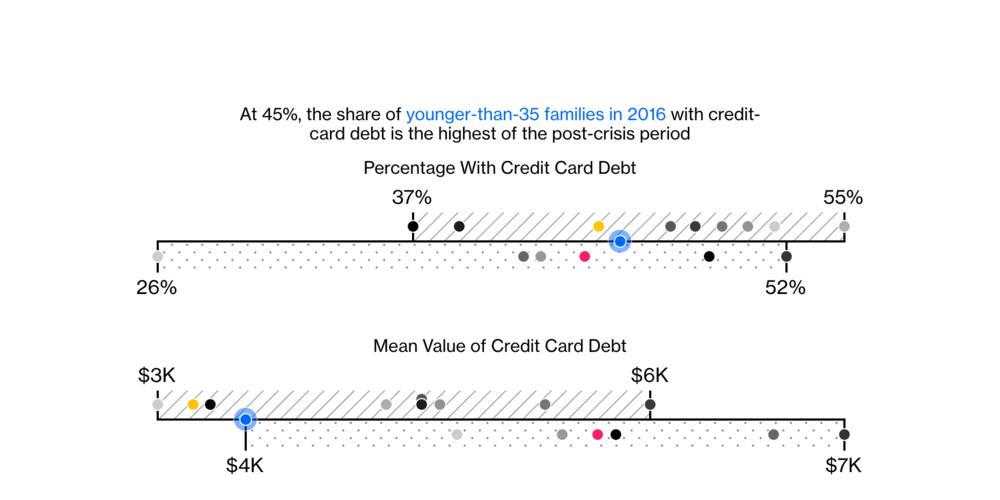

@hecharts The percentage of young people with car loans and credit-card debt is the highest of the post-crisis period. Neither is clearly a “good” or “bad” sign.

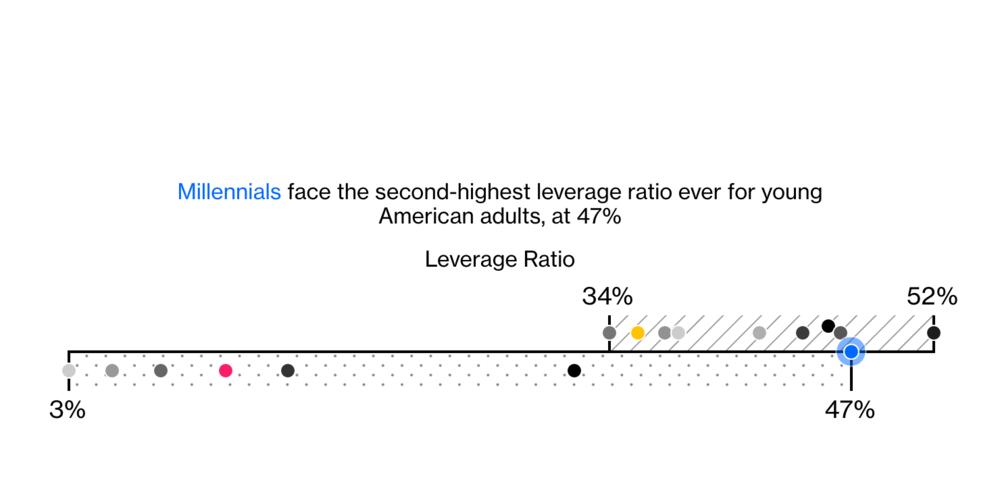

@hecharts In total, millennials are still saddled with the second-highest leverage ratio ever for young American adults, at 47%.

That’s a bit worrisome, especially given the record-low percentage of those with mortgage debt.

That’s a bit worrisome, especially given the record-low percentage of those with mortgage debt.

@hecharts So what’s the takeaway?

There’s no doubt millennials got off to a slower start than you’d otherwise expect. But it *seems* like they’re learning to deal with that.

For example, the fact that they’re putting money away in 401k plans is encouraging (even if it might be forced).

There’s no doubt millennials got off to a slower start than you’d otherwise expect. But it *seems* like they’re learning to deal with that.

For example, the fact that they’re putting money away in 401k plans is encouraging (even if it might be forced).

@hecharts Other areas, like homeownership, are noticeably depressed. But if millennials keep striving to improve their finances, it’s possible that we could see a bounce from those record lows. That, in turn, could provide a boost to the U.S. economy.

@hecharts Morgan Stanley is optimistic that millennials and Gen Z will carry the U.S. economy and stock market through the next decade.

Whether you agree or not, demographics matter. It’ll be the youth that make or break investing in the years to come.

The end.

bloomberg.com/graphics/2019-…

Whether you agree or not, demographics matter. It’ll be the youth that make or break investing in the years to come.

The end.

bloomberg.com/graphics/2019-…