,

10 tweets,

5 min read

Read on Twitter

1/ Don't misinterpret this as suggesting that a 60-65% market loss is typical for a bear market. Not at all. It would be the steepest decline since the Depression.

hussmanfunds.com/comment/mc1905…

hussmanfunds.com/comment/mc1905…

2/ The problem is that valuation metrics best correlated with *actual subsequent* full-cycle & long-term returns are just as elevated today as they were in 1929 and 2000. The Depression was basically TWO back-to-back 65% losses. The FIRST of those simply restored valuation norms.

3/ The fact is that even a brief return to historically run-of-the-mill valuation norms (or somewhat below, as we saw in 2007-2009) can wipe out years, or even decades of equity total returns, relative to T-bills.

4/ The thing that makes valuations easy to dismiss is that they can be utterly useless over extended segments of the market cycle. That's why it's critical to gauge speculative psychology w/ market internals. My biggest error in recent years was not taking that lesson far enough.

5/ While hypervaluation can be dismissed for extended periods, one needs the absence of ANY episode of risk-aversion to sustain them. Even Fed effectiveness is conditional. Investors may not recall that the Fed eased persistently the whole way down in 2000-02 and 2007-09.

6/ Over the complete cycle, even a brief return from hypervaluation to historically run-of-the-mill norms (not even undervaluation) can wipe out years, and even decades of equity total returns, relative to T-bills.

7/ While it may seem preposterous to suggest that current valuations exceed those at the 2000 peak, it's important to recognize how concentrated the hypervaluation in 2000 was in a single decile of stocks - generally large-cap glamour stocks.

8/ And that valuation skew was why I projected an -83% loss in tech stocks over the completion of the cycle. As it happened, that was the loss in the tech-heavy Nasdaq 100 by '02. Again, the reversion of hypervaluation to run-of-the-mill norms can be brutal over the full cycle.

9/ For the moment, despite hypervaluation, there are enough cross-currents that it still seems best for automatic safety nets and hard-negative views to kick in a bit lower than current levels. Investors remain keen to embrace narratives and it's best to allow for steep whipsaws.

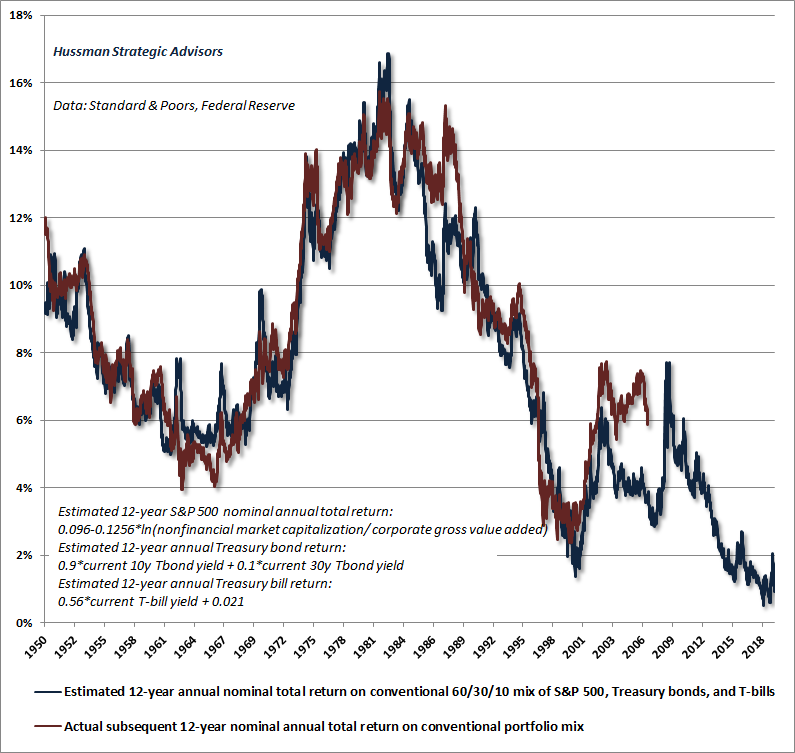

10/ Still, as @HowardMarksBook has often emphasized, it's essential to recognize where one is in the market cycle, even if short-term speculative pressures temporarily defer the consequences. At present, our estimate for a conventional 60/30/10 mix is near the lowest in history.