Good morning. Divergence b/n US & Asia is happening again w/ US ISM manufacturing bouncing in Jan to 50.9 from 47.8 while Asian data remains weak (Vietnam, Malaysia, Indonesia, Korea, Thailand, & China slower). New orders rose to 52! After an abysmal Monday China iron ore⏬today.

As mentioned yesterday, we only had that magnitude of single-day drops 5 times since 2001 & in 2007 markets rebounded the next day but NOT 2015. The drop of iron ore forebodes 2015 for today & not 2007, meaning, likely get to buy it cheaper if u think markets over-reacting🤗!

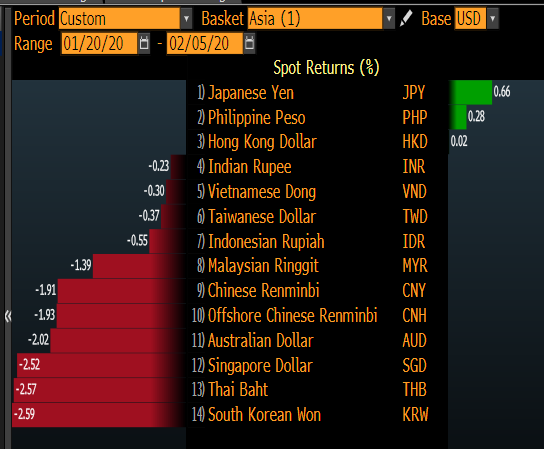

Link on US ISM manu if u want to read from the source (should always read primary data if u have access to interpret data urself). Asian data below. B/c of this, USD rising to 97.8 (note this is just w/ major floaters & mostly EUR & doesn't include CNY)

instituteforsupplymanagement.org/ISMReport/MfgR…

instituteforsupplymanagement.org/ISMReport/MfgR…

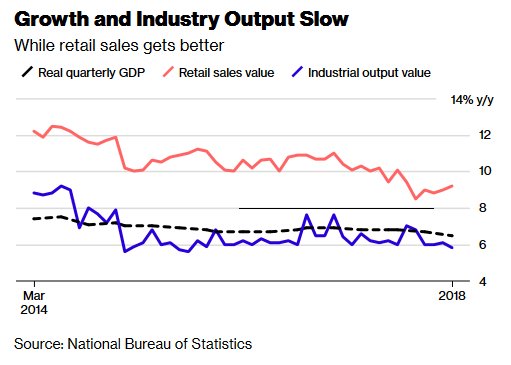

China's fix is 6.9779 & likely an indication to put a floor on this depreciation expectation. Note that the Phase 1 deal doesn't include pandemic so defo can be a tool to offset weakness. Lackluster activity also means Q1 GDP very weak & question is whether Q2 impacted.

Busy wk!

Busy wk!

OK, best is to do short-term & wrap around some key ideas on who can stomach this virus/China spillover in Asia.

Lots of central bank decision this wk & RBA is today & markets expect a HOLD of 0.75% due to an already weak AUD (down to .669) & OK employment. Some calling for cuts

Lots of central bank decision this wk & RBA is today & markets expect a HOLD of 0.75% due to an already weak AUD (down to .669) & OK employment. Some calling for cuts

Like expectations, China opens DOWN but magnitude smaller than yesterday. Iron ore foreshadowed. Note that security lending was stopped yesterday in China & so the decline of equities add to the tightening of liquidity conditions onshore & will hurt those w/ repayment pressure.

S&P stated that China bank NPL ratio could exceed 6% on virus as earnings FALL & so help needed in terms of rolling over debt & also access to financing to cover the decline of earnings in the short-term. Note that China is very short-term financing dependent.

Watch real estate

Watch real estate

According to Natixis corporate monitor, real estate H1 EBITDA/interest expense was only 2.6 & so lower than global peers of 4.6 & so Chinese real estate is one to watch & question is how will the PBOC liquidity injection'll find its way to these firms.

Key are the following:

Key are the following:

a) Need this virus to peak soon - some estimate early Q220 so not good so need this to be contained to Q1 & longer this lasts it strikes at weak corporate balance sheets

b) Key is policy support, not just broad but targeted.

S&P expects NPL to tripple!

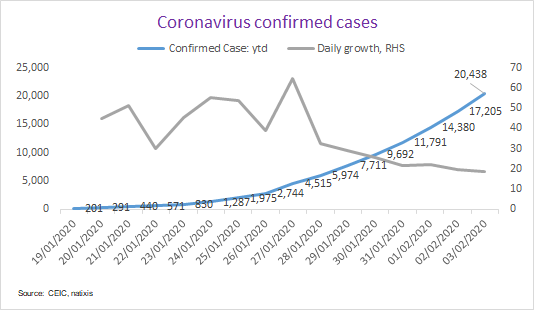

Ready? Here are some charts for you for #coronavirus . Confirmed cases & daily growth rates. We're now at 20,438 & growth rate of 19% (rate of growth slowing but base higher so compounding at a slowing but high rate).

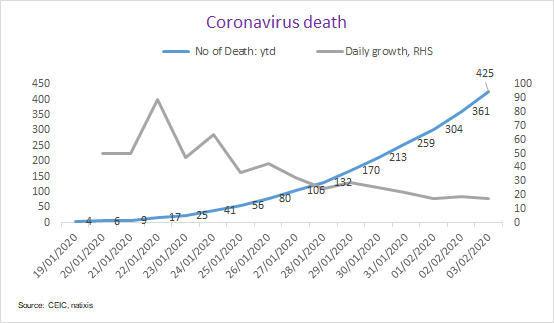

#coronavirus deaths (only official) & growth rates. Note that it's now 425 & growth rate slowed to 18%

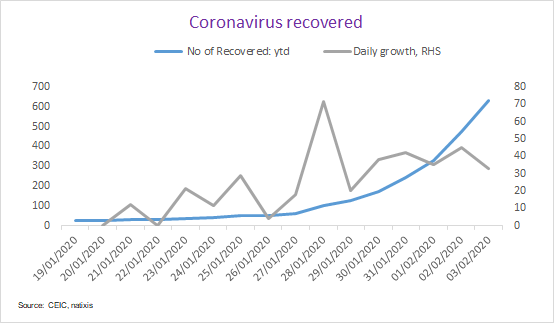

This is kind of encouraging & worrying. The # of people recovered from the #coronavirus is now 632 & seems like growth rate stagnating & so that means 19,806 haven't recovered???

Not sure about this stats...

Not sure about this stats...

OK, I did some simple forecasting (assuming daily confirmed cases, deaths GROWTH SLOWING), then we get in three days about 37.7k confirmed & 756 deaths.

Note that this growth is exponential on a daily basis even if slowing. This doesn't assume higher growth rates but slower...

Note that this growth is exponential on a daily basis even if slowing. This doesn't assume higher growth rates but slower...

Assumption of slowing daily growth rates gets us roughly ~40k by end this wk & deaths around ~800 by end of the wk. By next wk, it depends whether people go back to work vs staying home this wk.

Btw, HK just reported a death on the virus so we'll see the external death ratio.

Btw, HK just reported a death on the virus so we'll see the external death ratio.

Note that during SARs the mortality ratio was higher outside the mainland than inside. We'll see more.

Urgh, now I see why my family was like why are you leaving California to go to Hong Kong.

WEAR YOUR MASKS!!! 😷😬

Urgh, now I see why my family was like why are you leaving California to go to Hong Kong.

WEAR YOUR MASKS!!! 😷😬

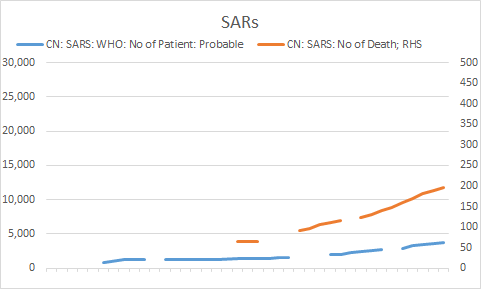

Are you ready? Here we go. Comparison b/n SARs vs Corona for mainland deaths + confirmed cases.

Btw, deaths in the mainland already exceeds SARs & confirmed cases exceeding by a WIDE MARGIN.

So the economic impact'll be WORSE (also China bigger & retail etc more key now).

Btw, deaths in the mainland already exceeds SARs & confirmed cases exceeding by a WIDE MARGIN.

So the economic impact'll be WORSE (also China bigger & retail etc more key now).

Facts on SARs & #coronavirus :

* SARs TOTAL deaths in mainland 348 vs 425 by 3 Feb 2020 of coronavirus; if the rate of death slows, we'll double SARs by the end of this wk alone;

*SARs mainland infected total was 5,327 vs 20,438 on 3 Feb 2020 for corona or roughly 4 times that!

* SARs TOTAL deaths in mainland 348 vs 425 by 3 Feb 2020 of coronavirus; if the rate of death slows, we'll double SARs by the end of this wk alone;

*SARs mainland infected total was 5,327 vs 20,438 on 3 Feb 2020 for corona or roughly 4 times that!

So if u reading macroeconomic research & someone tells u that the economic impact of this is LESS THAN SARS, then you have to consider that: By now, schools etc during SARs weren't closed & the infected & deaths were lower. Also China was smaller & retail etc was smaller % of GDP

Here is the chart of corona virus after 1 month:

19 Jan to 3 Feb

19 Jan to 3 Feb

SARs 27 March 2003 to 4 May 2003

Much much lower infection # & rate as it was less infectious.

Much much lower infection # & rate as it was less infectious.

SARs peaked roughly about May 2003 so if the paper I posted yesterday is correct & coronavirus peaks around April then we'll look at Q2 2020 economic impact & not just Q1

👇🏻👇🏻👇🏻

👇🏻👇🏻👇🏻