,

55 tweets,

13 min read

Read on Twitter

1/ THREAD: Trump’s signing his EO tomorrow. Here’s how it can destroy the Individual Market: acasignups.net/17/10/10/how-t… #ACASabotage

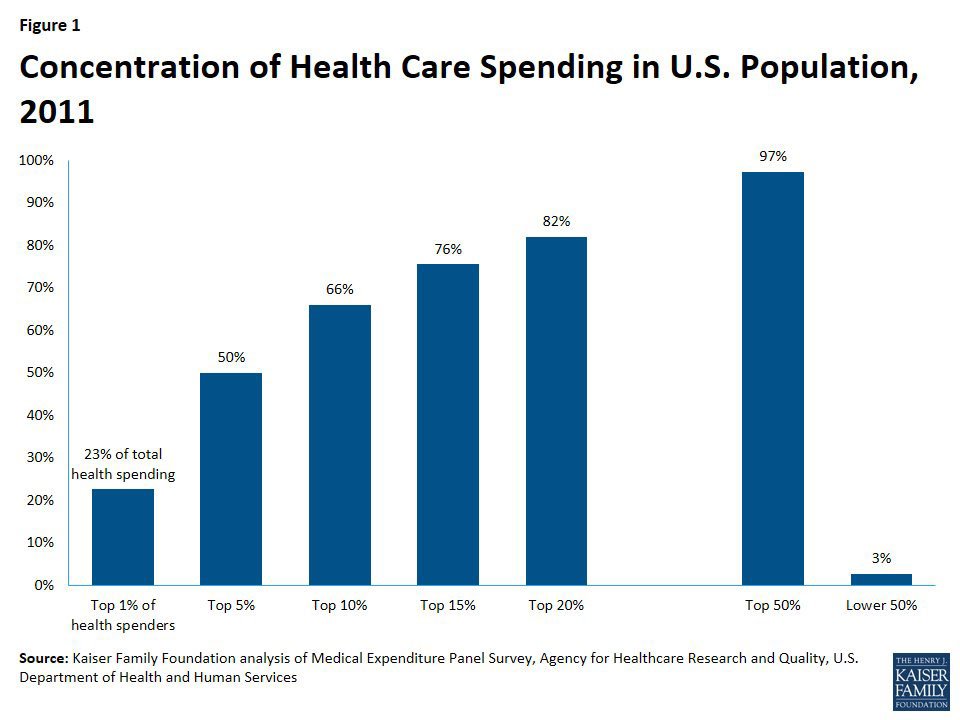

2/ Here’s the breakout of how healthcare spending is concentrated nationally, according to @KaiserFamFound :

3/ As you can see, 1% of the population accounts for 23% of all healthcare spending. Think cancer patients undergoing chemo, etc.

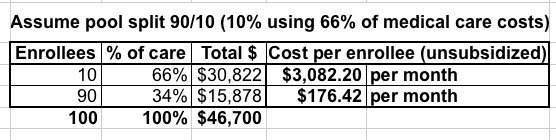

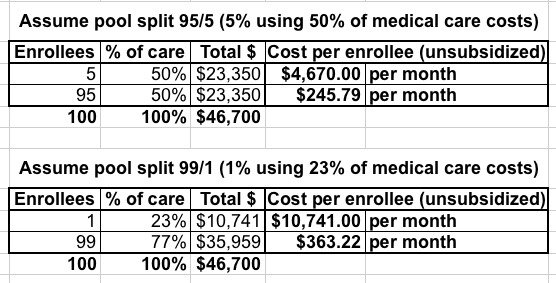

4/ 5% accounts for 50% of all spending. 10% accounts for 66%. 20% accounts for 82%, and 50% of the pop. accounts for 97% of ALL spending.

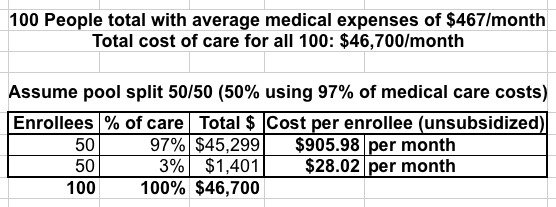

5/ Let’s say you have 100 people who collectively rack up ~$47,000/month in healthcare costs (avg. #ACA policy premium is ~$467 this year).

6/ (Not worrying about deductibles, co-pays, etc etc; this is for illustrative purposes only).

7/ Let’s also assume all 100 are enrolled in the same benchmark Silver plan to keep it simple.

8/ And finally, also to keep it simple, assume they’re all the same age & live in the same area.

9/ OK, so all 100 are paying (before subsidies) around $467/month. Half of them earn <400% of the fed. poverty line, half earn more.

10/ The 50 who earn <400% FPL are subsidized on sliding scale, so let’s say 5 are paying nearly full price (not thrilled but tolerate it)…

11/ …while the other 45 are more generously subsidized & paying much less (say, $50 - $350/mo depending) after subsidies. They’re happy.

12/ Meanwhile, the *other* 50 who earn MORE than 400% FPL (around $48K+ for an individual) are all paying full price. They’re grumbly.

13/ OK, so Trump’s EO *keeps* #ACA exchange plans (which require full EHB coverage, guaranteed issue, community rating, etc etc) in place…

14/ …but also removes restrictions on “association plans” and allows “short term” plans to become year-round.

15/ Since #ACA regulations (EHBs, guaranteed issue, comm. rating) don’t apply to association/short term plans, they’re dirt cheap, right?

16/ OK, so anyone who a) earns >400% FPL and b) doesn’t have some expensive ailment flocks to the Short Ass Plans.

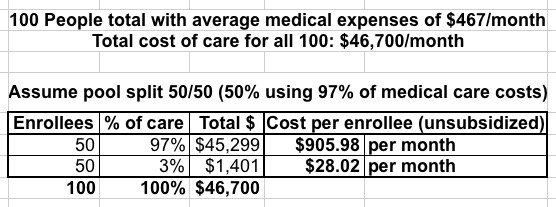

17/ (yes, I’m calling these #ShortAssPlans. I’m 12 years old at heart)

18/ Meanwhile, anyone who earns <400% FPL *or* who earns more but needs the protections of full EHBs/etc sticks with #ACA plan.

19/ So now, anyone who’s subsidized + anyone w/pre-existing cond. is on exchange. Anyone who’s higher income/healthy goes to #ShortAssPlans.

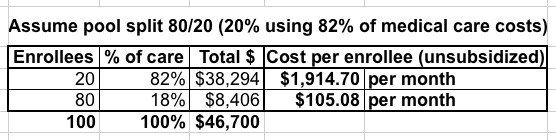

20/ What does that look like? Well, remember, 50% of pool = 97% of the cost. That looks like this:

21/ The #ShortAssPlans only cost $28/month, woo-hoo! Those folks are thrilled! Unfortunately, the #ACA plans now cost $906/mo unsubsidized.

22/ The good news is that most of these folks are heavily subsidized. The bad news is some of them aren’t. They can’t afford full price.

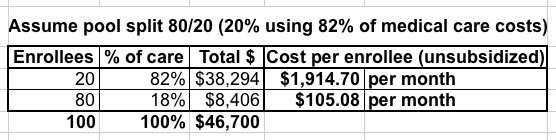

23/ …so the remaining unsubsidized (or only lightly subsidized) shift to #ShortAssPlans. Eventually we have something like this:

24/ Now the #ShortAssPlans cost $105/mo. That’s a lot more than $28 but still quite reasonable. Unfortunately, #ACA plans are now $1,900/mo.

25/ By now, the ONLY way to afford an #ACA plan is if you’re HEAVILY (and I mean heavily) subsidized. EVERYONE unsubsidized drops out.

26/ At this point the #ACA exchanges have been turned into a de facto High Risk Pool. As long as it’s properly funded, that MIGHT work…

27/ …for everyone UNDER 400% FPL (assuming every carrier hasn’t dropped out of the exchanges altogether by this point). Meanwhile…

28/ …the #ShortAssPlans are still pretty cheap, hooray! Everyone over 400% FPL is happy, right? Except for one little problem…

29/ What happens when someone earning >400% FPL on a #ShortAssPlan is diagnosed with something not covered by it? Ut oh.

30/ Let’s say you earn $60K/year (around 500% FPL), you’re on a #ShortAssPlan and are diagnosed w/cancer, diabetes, whatever.

31/ Your dirt-cheap #ShortAssPlan doesn’t cover your expenses (that’s what makes it dirt-cheap). So assuming you survive until Nov. 1st…

32/ …you can switch to an #ACA plan which HAS to cover it, right? Except you earn $60K, so you have to pay full price.

33/ Remember, at this point “full price” on the #ACA exchange would be $1,900/mo. That’s $23K/year on a $60K income…

34/ …which you probably aren’t earning anymore anyway because you have cancer now and can’t work.

35/ …which, is just as well, actually, because the only way to get subsidies is for your income to also drop BELOW 400% threshold anyway.

36/ In short, if it went through (AND survives legally AND the carriers actually stick around the exchanges)…

37/ …it would create not one, not two but THREE effectively separate risk pools: insanely⬆to treat, heavily subsidized exchange enrollees…

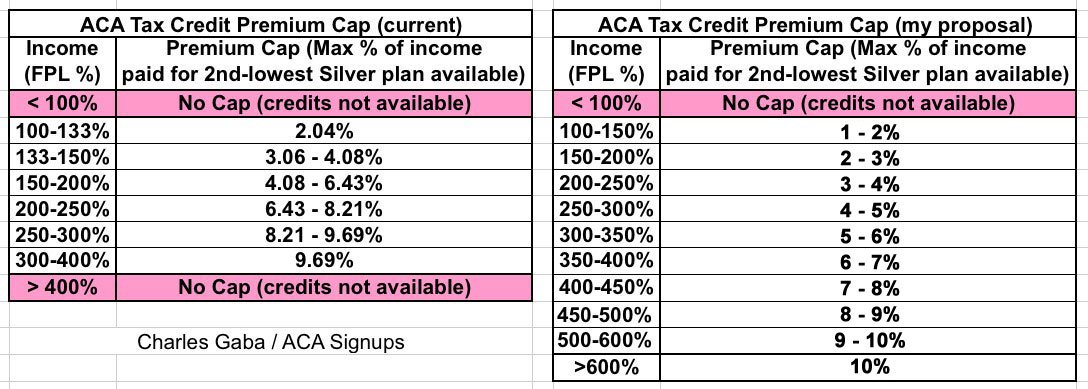

38/ …fairly ⬇to treat, high-income #ShortAssPlan enrollees…

39/ …and middle/high-income people w/expensive conditions who would be UTTERLY screwed w/no place to turn.

40/ This would include people like @lpackard…but it *could* include ANYONE who earns >400% FPL sooner or later.

41/ Of course, there’s a simple solution to most of this problem: REMOVE THE 400% CAP ON TAX CREDITS.

42/ That wouldn’t solve everything, of course, but it’d resolve a big chunk of it. A good 4-8M people >400% FPL…

43/ …would get a Silver #ACA plan (w/full protections) for no more than 10% of their income: acasignups.net/17/07/25/updat…

44/ But here’s the larger point of all this: Here’s those tables again (50/50, 80/20, as well as hypothetical 90/10, 95/5 and 99/1):

45/ Do you notice anything about all of them? THE TOTAL COST OF HEALTHCARE FOR THESE 100 PEOPLE REMAINS THE SAME NO MATTER WHAT.

46/ Slicing people up into different risk pools in & of itself does NOTHING to actually reduce the actual total *cost* of healthcare.

47/ And in fact doing so goes completely against the very CONCEPT of health insurance: Pooling Risk. /end.

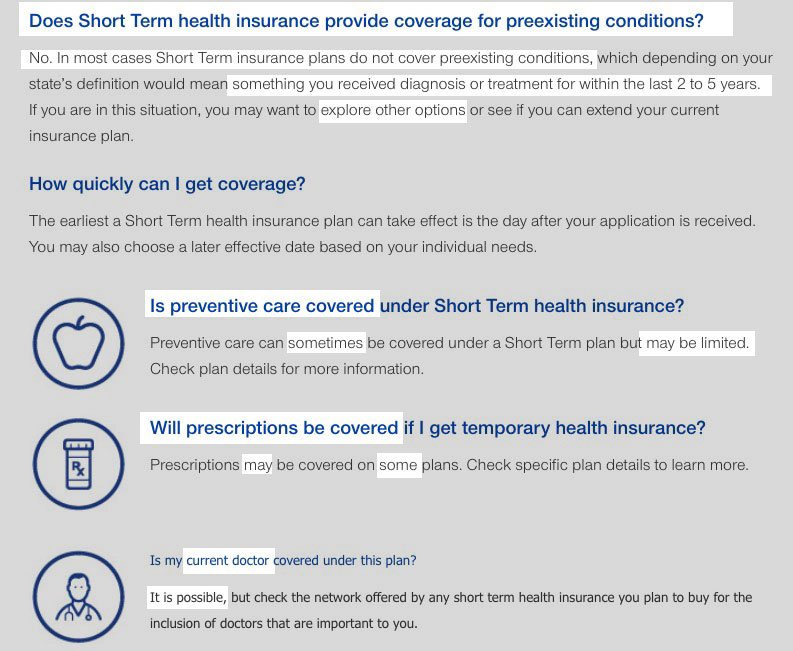

P.S. One more thing: Short-term plans *as they stand now* aren’t necessarily all bad; they do serve a need for some situations. HOWEVER…

…here’s an example of why they’re useless for anyone w/a serious problem: uhc.com/individual-and…

I should also clarify one other important point: High Risk Pools are NEVER properly funded, BECAUSE they’re so insanely expensive. /end2

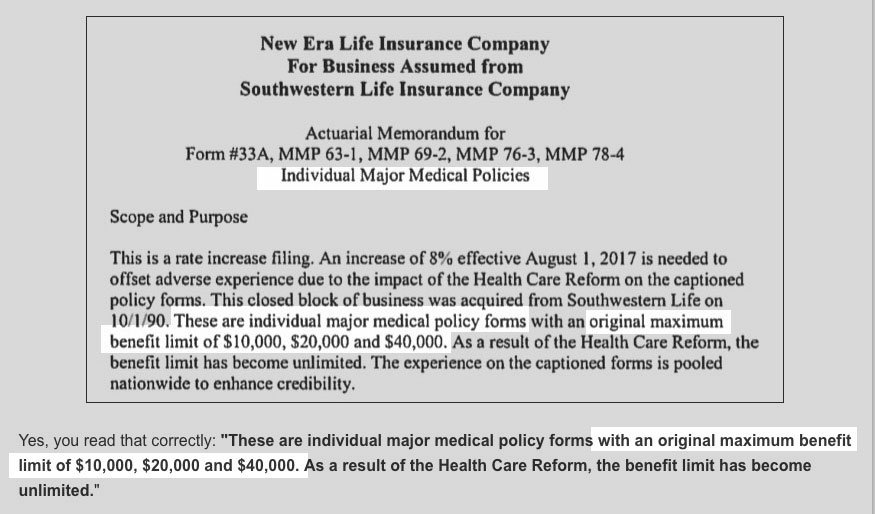

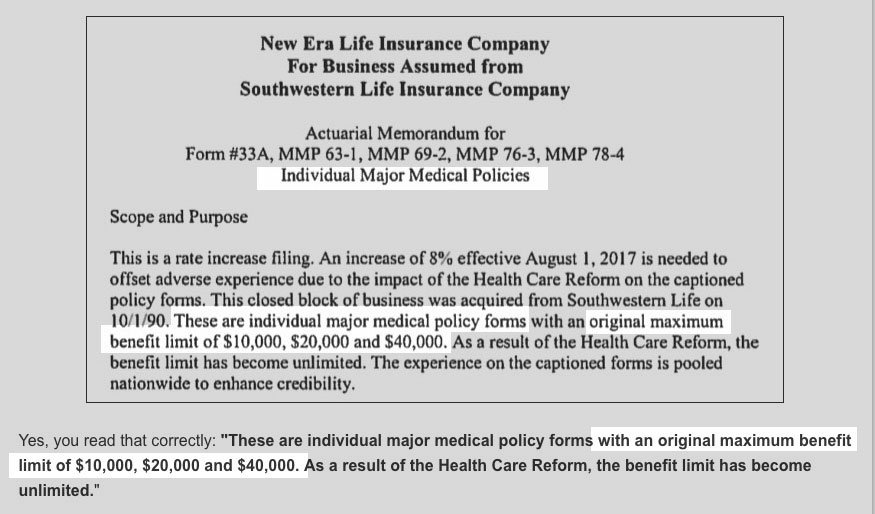

RELATED: Here’s the type of policy which used to be offered on the individual market as a “major” medical plan:

Yet Another PS: Here’s an example of the type of “major” medical plan which used to be typically available: acasignups.net/17/05/29/some-…

$10K-$40K/year in maximum benefits? Awesome! That’s enough for…one day in the neonatal unit for a premature infant? A single chemo session?

OK, I won’t say /end this time, I’ll leave it open-ended, since there’s so much more to say about this insanity…but /end for the moment…

While I’m at it, for what it’s worth...