,

24 tweets,

11 min read

Read on Twitter

📣 THREAD, WITH TABLES & GRAPHS! 1/

A Really Deep Dive into #MedicareForAmerica: acasignups.net/19/05/02/reall…

A Really Deep Dive into #MedicareForAmerica: acasignups.net/19/05/02/reall…

So yesterday, @RosaDelauro & @RepSchakowsky re-introduced their #Med4America universal healthcare coverage bill. It’s important to note that BOTH of them are members of the Congressional Progressive Caucus, and Schakowsky is also a co-sponsor of the House #MFA bill. 2/

@rosadelauro @RepSchakowsky In other words, this is NOT a battle between “progressives” and “centrists”. #Med4America is *very* progressive…while also, in my view, simply being more practical than the “pure” #MFA bills. It starts out as a robust Public Option for 2 yrs, but then becomes MUCH more. 3/

@rosadelauro The simplest way I’ve found to describe how it works once it’s ramped up is this:

It’d be mandatory for the 1/2 of the country least likely to have a problem with it being mandatory…and optional for the 1/2 of the country most likely to want it to be optional. 4/

It’d be mandatory for the 1/2 of the country least likely to have a problem with it being mandatory…and optional for the 1/2 of the country most likely to want it to be optional. 4/

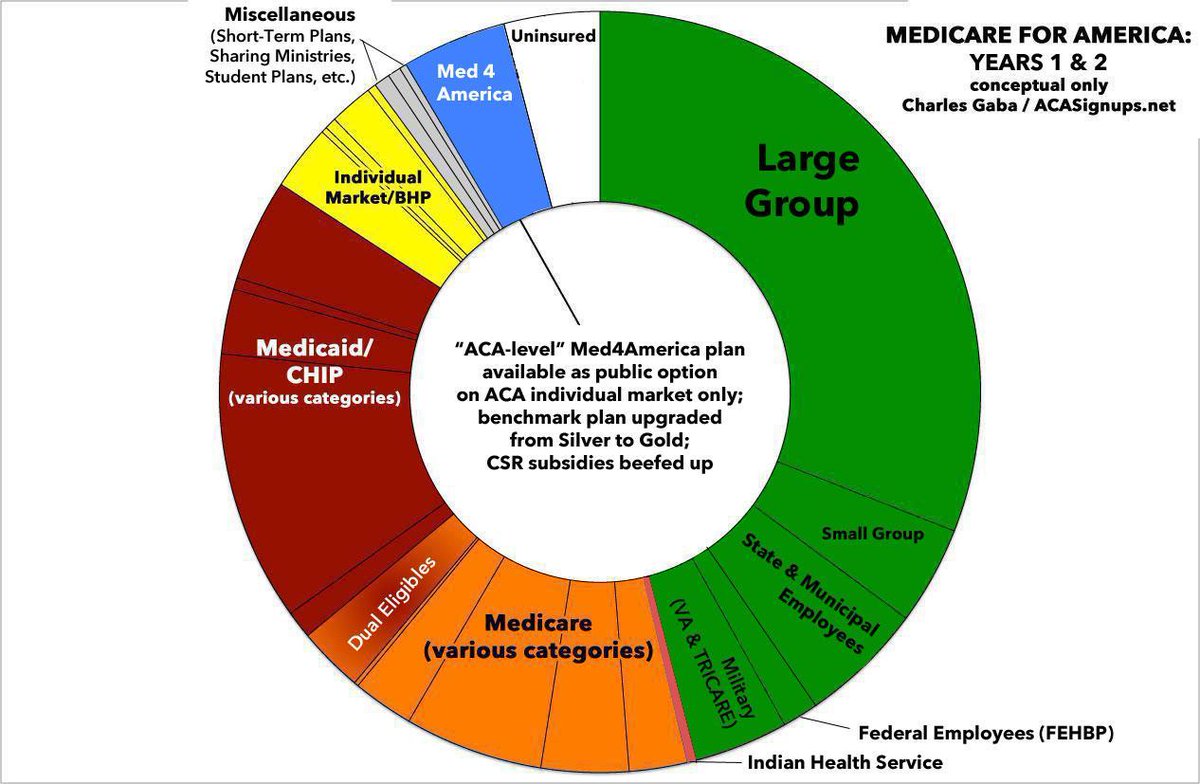

OK, so here's how the timeline would work. First of all, once again, here's what the current total U.S. population healthcare coverage landscape looks like today (this is actually from 2 years ago, but it should still be pretty close): 5/

For the first 2 years, #Med4America would operate mostly as a combination #ACA2.0 upgrade plus a robust public option on the existing #ACA exchange, with beefed-up/expanded premium subsidies & CSRs. 6/

The first 2 years would give time for the government, carriers, hospitals, doctors, advocates, etc. to prep for the main launch in Year 3. This is the point when current Medicare enrollees, ACA exchange enrollees, junk plan enrollees and the uninsured would be phased in. 7/

Year 3 is also when auto-enrollment of newborn babies & new 65-year olds would start. Small biz could also OPTIONALLY transfer employees over to #Med4America *or* they could keep private coverage *as long as it's Gold-level or higher*. OR employees could move on their own. 8/

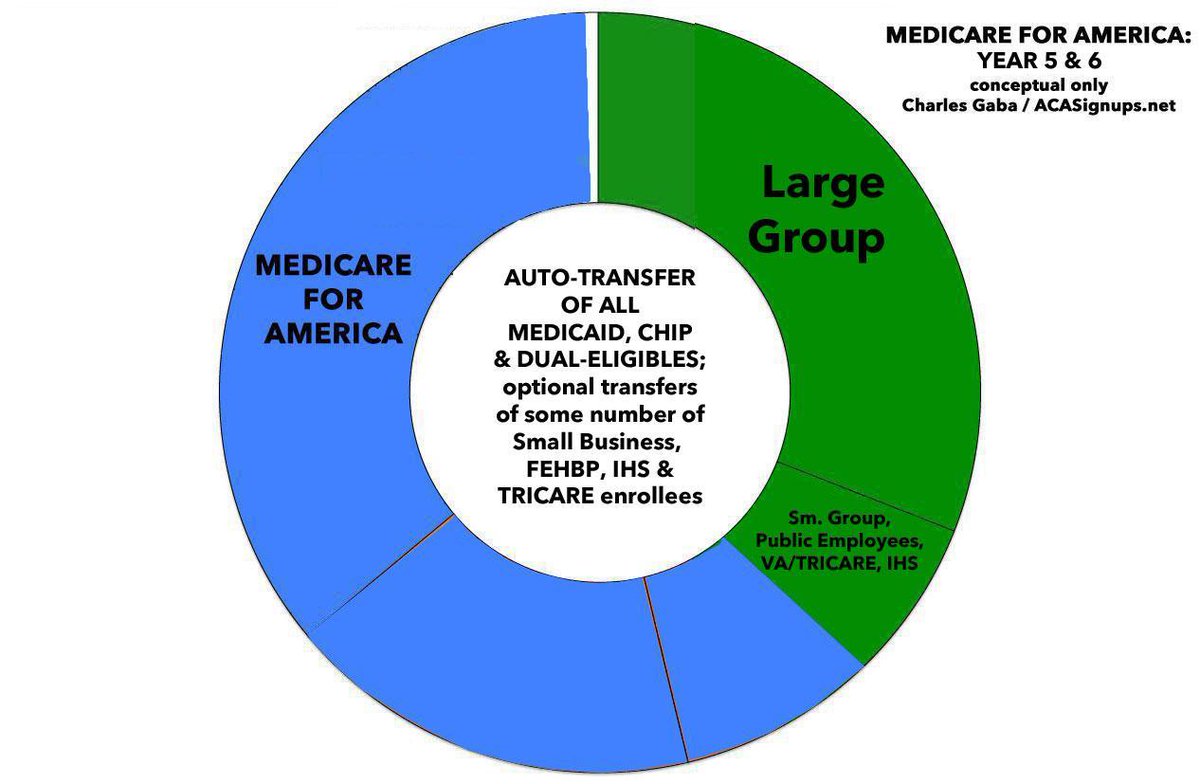

Year 5 is when the existing Medicaid/CHIP population would be absorbed into the #Med4America system. At this point a significant chunk of small business employees would presumably have *chosen* to make the move, as well as those normally covered by FEHBP, TRICARE & IHS. 9/

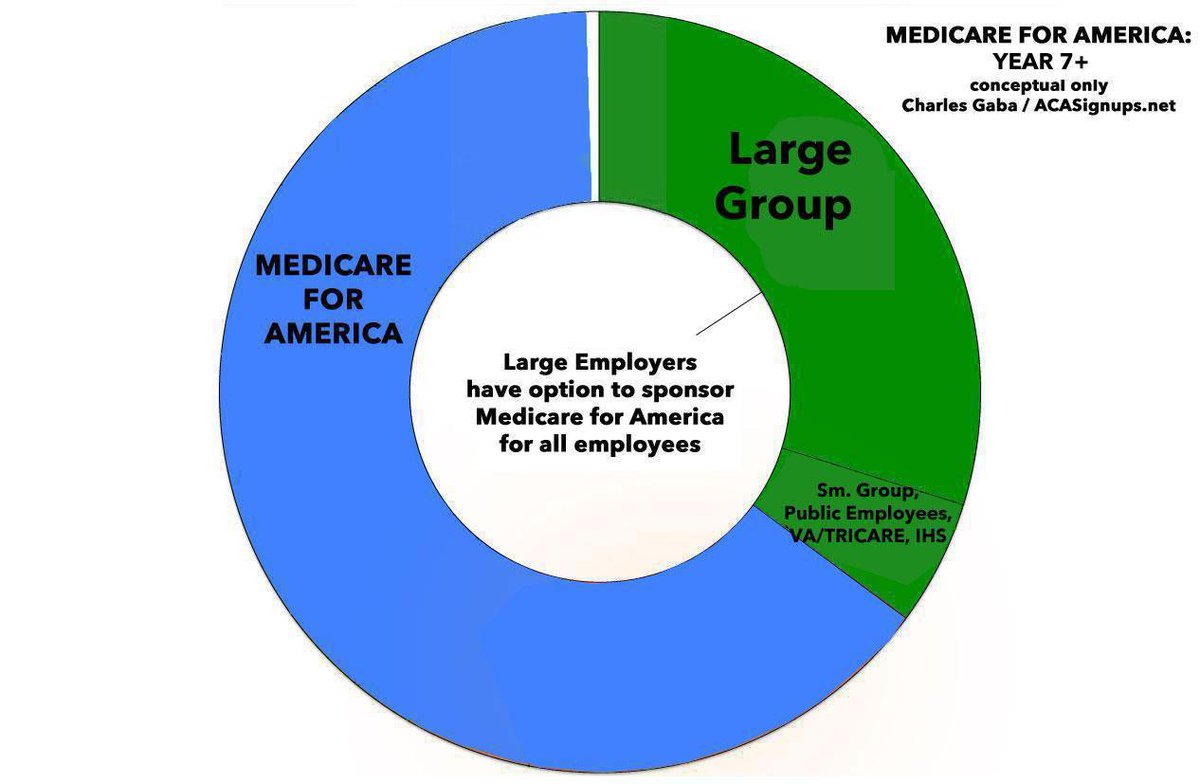

Finally, when the dust has settled on all of that, starting in Year 7, *large* employers would have the *option* of either a) keeping Gold-level or better private insurance *or* b) transferring employees over to #Med4America & paying a flat 8% payroll tax. 10/

What if you're an employee of a large business who wants to move to #Med4America but your employer doesn't want to move everyone? YOU CAN STILL DO SO, and pay no more than you are now, for *much* better coverage. Your employer would still pay what they're paying now as well. 11/

From that point on, roughly 2/3 of the total U.S. population would be enrolled in #Med4America, while the other 1/3 would be on *high quality* private employer insurance. After that it would depend on the decisions of employers and/or employees. 12/

How much would it cost? Well, for those earning <200% FPL (~$25K if you're single, $51K for a family of four), it would cost...nothing. Zilch. No premium, no deductible, no co-pay, nothing out of pocket, 100% actuarial value. 13/

What about those over 200% FPL? Well, there'd be NO DEDUCTIBLES for them either...the only costs would be premiums and (truly) reasonable out of pocket costs, both on a sliding scale. Here's my estimates based on the legislative text: 14/

How much would this be in real dollars?

Let's say you're single and earn $30,000/year. That's around 240% FPL.

Your premiums would be around 1% of your income, or $25/month. NO deductible. Maximum out of pocket costs likely around $400. Worst-case scenario: $700 for the year.

Let's say you're single and earn $30,000/year. That's around 240% FPL.

Your premiums would be around 1% of your income, or $25/month. NO deductible. Maximum out of pocket costs likely around $400. Worst-case scenario: $700 for the year.

What if you're single and earn earn $50K? That's ~400% FPL. Your premiums would likely be around 4% of income, or $167/month. No deductible. Max OOP of perhaps $1,600, for a worst-case scenario annual cost of around $3,600 no matter what. 16/

OK, what about if you earn $80,000/year? That's 640% FPL. Your premiums would max out at 8% of income, or $533/mo. Again, NO DEDUCTIBLE. Maximum OOP of $3,500. Absolute worst-case scenario: $9,900 at most. 17/

So what's *covered*? Here's where it would be very similar to Bernie/Jayapal-style #MFA: Pretty much everything...all ACA essential health benefits, plus dental & vision, and yes, *full reproductive services*. One thing MFA & Med4America agree on is it's time to tackle Hyde. 18/

What else? Well, it's a long list, but the most important bragging point is that #Med4America was the first of the current batch of healthcare reform bills to include LONG-TERM SUPPORT & SERVICES. #LTSS is a *huge* deal. The MFA bills added it after #Med4America did. 19/

How would it be paid for? Unlike the #MFA bills which don't include funding mechanisms within the bill itself, #Med4America is *very* specific:

--repeal GOP tax bill

--5% surtax on income > $500K

--increase Medicare payroll tax on income > $200K

20/

--repeal GOP tax bill

--5% surtax on income > $500K

--increase Medicare payroll tax on income > $200K

20/

--increase the Net Investment income tax for income > $200K

--increase excise taxes on tobacco, alcohol & sugary drinks.

Notice that only 2 of these bullets impact anyone earning less than $200K at all: Repeal of the GOP tax bill and the tobacco/alcohol/sugary drink taxes. 21/

--increase excise taxes on tobacco, alcohol & sugary drinks.

Notice that only 2 of these bullets impact anyone earning less than $200K at all: Repeal of the GOP tax bill and the tobacco/alcohol/sugary drink taxes. 21/

What about Medicare Advantage? I'm not a fan of it, but a lot of people are, so they're keeping it as an option...HOWEVER, it would be subjected to much tighter regulation than today, and would have to be at least as comprehensive as official #Med4America. 22/

There's a ton of other stuff including a smart Medical Student Loan Debt Forgiveness provision. Check it out here: 23/

acasignups.net/19/05/02/reall…

acasignups.net/19/05/02/reall…

And finally: I spent like 10 hours working on this analysis today. If you find it useful and are in a position to do so, please consider supporting my work, thanks! acasignups.net/donate