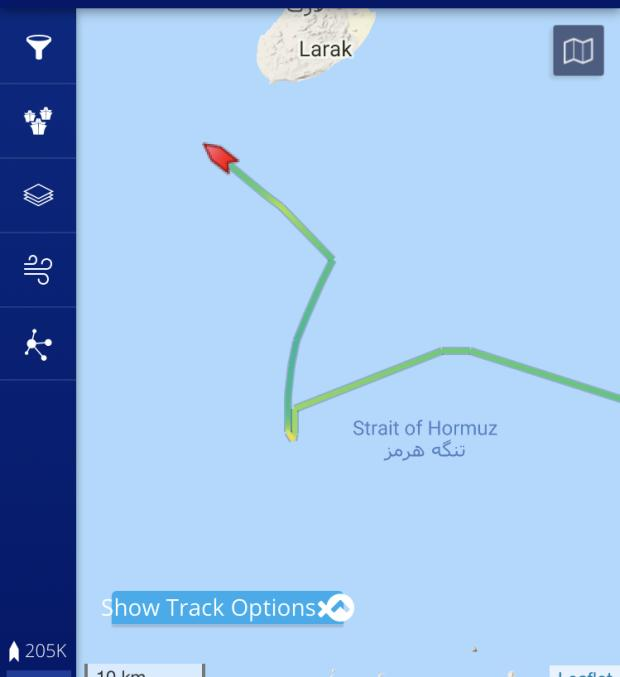

UK company Diaceutics #DXRX that is an picks and shovels play on precision medicine. The company is growing fast, profitable, to me reasonably cheap and unknown: 6 posts in 2 years from wise sages of ADVFN. The market they're working in is the future and has started to arrive.

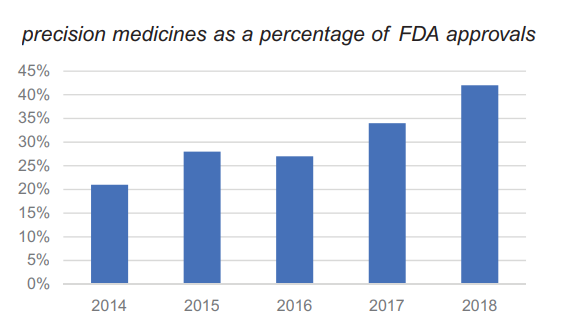

Precision meds are those which only work on certain groups of individuals. 2 main issues arise beyond normal drug therapies: you need to test on the right people and if successful you need to find the people who can benefit from it - and pay you - before your patent runs out.

All these meds require diganostic tests. Ever since Herceptin for breast cancer came out in 1998, launching without full developed tests has been an issue for patients and industry. Patients either get nothing or duds and industry loses sales in their window of exclusivity.

This is where #DXRX comes in and there are two angles to this: their existing business which I think is worth the price alone and the new one they're developing, which is potentially exciting.

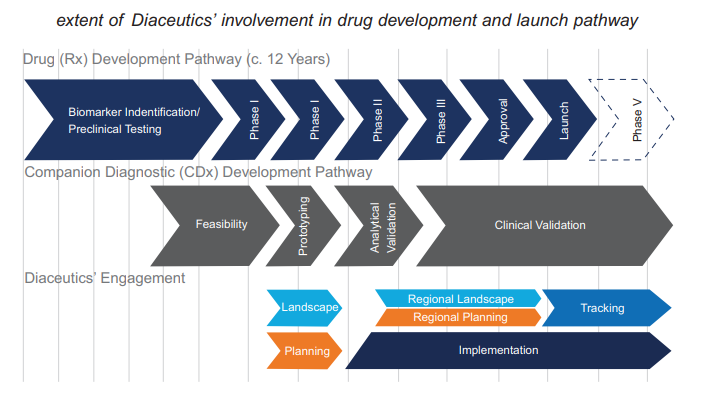

This picture illustrates what they do now

This picture illustrates what they do now

They identify the labs and patents for testing both at drug development stage and once in the market. There are nearly 200 drugs which require this, 800 in development and the company expects the market to expand 5-fold in 3 years.

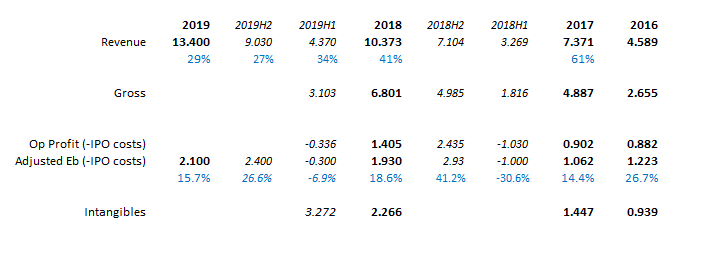

Here are the numbers on this existing business

Here are the numbers on this existing business

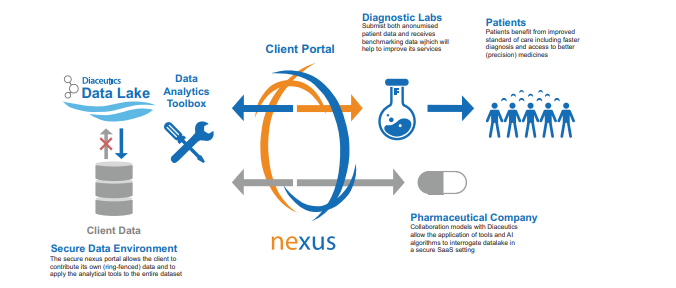

The second angle is that they're putting this into software they're developing. The labs will input the data from tests, other labs can benchmark against it. The data will be provided to pharma and doctors. Expected live this year, revenues 18-24 months later. Called Nexus

At an £80M cap, ex-cash of 10 or so it's about 5x this year's sales, 4x next for a company which once the numbers settle down should be doing around 20% operating margin with strong growth, in the reliably expensive life sciences market. Nexus could also be promising.

It's small, there's competition from CROs, other consultancies and it has large clients over 10% of revs - 3 in 2018. However they service a real need, in a growing market and to my mind, could turn out to be rather cheap here.

And finally, here's what a typical lab looks like.

And finally, here's what a typical lab looks like.