Restructuring Lebanon's FX debt (eurobonds) is a necessary, but not sufficient, condition for putting debt on a sustainable footing. Negotiations with bondholders is just one piece of the puzzle – even an aggressive haircut (principal+interest) won’t create a big enough dent

For the debt ratio (160% of GDP, o/w 60% in USD and 100% in LBP) to actually budge, a plan needs to encompass restructuring the massive internal (LBP) debt, restructuring the BdL’s CDs, and, by extension, recapitalising the banks.

See @Mohdfaour89 earlier work on this

@Mohdfaour89 Let’s not forget the real elephant in the room here. On the FX side, banks are owed even more in USD CDs by the BdL (~$21bn) than they are owed in Eurobonds by the MoF (~$15bn).

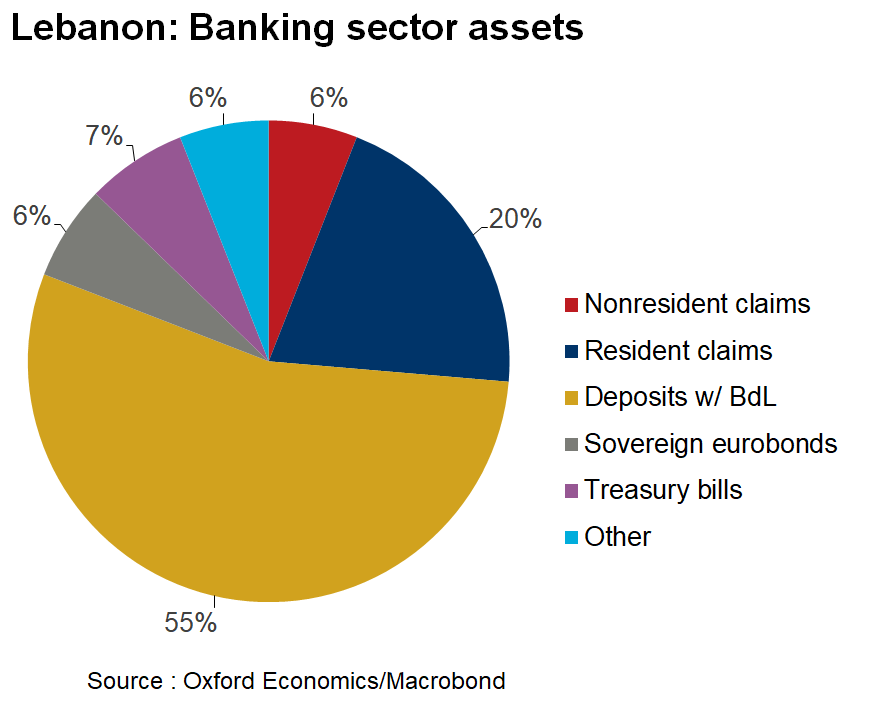

@Mohdfaour89 Remember also that, in their infinite savviness, banks locked up 70% of their assets in exposures to the sovereign and BdL. In fact, their Eurobond exposure is only a small part of that. See Chart. A full 55% of their assets are deposits with BdL! Let that sink in for a second.

@Mohdfaour89 Nevertheless, a 50% haircut on EBs would wipe out almost a third of banks’ capital. Assuming also a 50% haircut on USD CDs owed by the BdL, then banks' capital is almost entirely wiped out, without even considering the likely rise in NPLs from last reported figure of 18%

@Mohdfaour89 We know this. Crucially, creditors know this too. Which is why, on the face of it, negotiations with EB creditors will look like they are about debt reduction, but they are really going to be about burden-sharing.

@Mohdfaour89 Foreign creditors will expect Lebanon to share the cost of adjustment. And the only other way to bring down the debt ratio will be to impose an inflation tax on local debt and local depositors. Given the size of the financial hole, the haircut on Eurobonds is almost a sideshow

@Mohdfaour89 No matter how you spin it, the temptation to inflation the local portion of the debt away will be too big to resist. With growth unlikely to recover meaningfully given the weight of debt, expect negative real rates and capital controls for a long long time

@Mohdfaour89 The sooner we come to terms with this, the sooner we can have constructive negotiations with external creditors and a plan to deal with the internal ones. And the sooner we realise that restructuring EBs on their own is not the magic bullet