Inflation data for July moderated somewhat, at least relative to the heady pace of recent months, which should temper #market and policymaker concerns a bit, despite the fact that #inflation will stay sticky-higher for a while and the #risk remains to the high-side.

Core #CPI (excluding volatile food and #energy components) came in at 0.3% month-over-month and 4.3% year-over-year, a bit less than the consensus forecast, and headline CPI data printed at a solid 0.5% month-over-month and came in at 5.4% year-over-year.

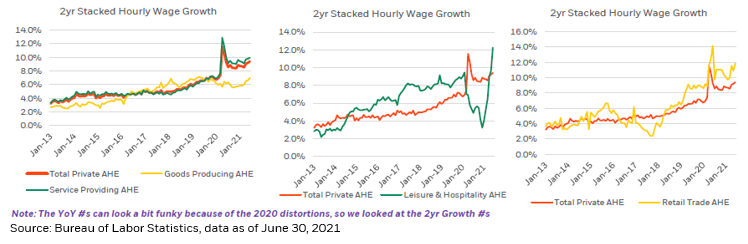

While we think that it’s hard to see a case for the recent levels of elevated #inflation turning into “1970s style” runaway price increases, higher #wages and elevated growth for an extended period will allow companies to achieve higher levels of #PricingPower for a time.

Still, in the long run #productivity enhancements that corporations put into place should ultimately dull future #inflation, and while wages and prices saw strong #correlation in the 1970s and 1980s, by the early 1990s that relationship was breaking down in a profound way.

However, intentionally late #policy adjustments, as the #Fed’s Average Inflation Targeting goals may end up being, can create distortions in the #economy and #markets that (ironically) risk undermining the very successes that policy has achieved up to this point.

Additionally, overly easy #MonetaryPolicy can worsen societal #income and #wealth gaps, and interestingly, those periods in which income gaps have closed most dramatically have tended to be almost exclusively after Fed rate policy has normalized.

As a result of all this, we think the #Fed should adjust monetary policy away from emergency conditions, as these policies are now distorting the economy and #markets.

• • •

Missing some Tweet in this thread? You can try to

force a refresh