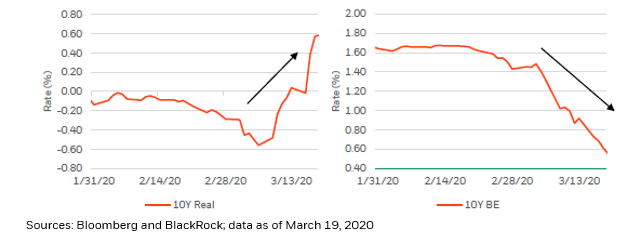

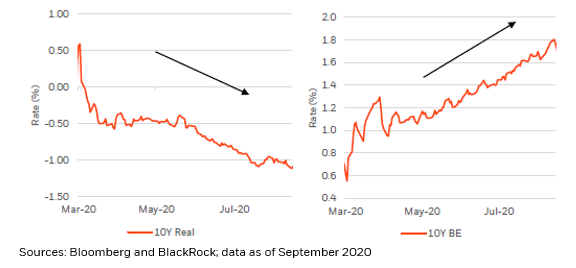

Today’s robust #inflation data surprised in its strength and will likely persist in the short-run, and in some areas the intermediate-term, although we think that long-term the @federalreserve is largely correct in identifying real #economy price gains as mostly #transitory.

Much of today’s #inflation is due to reopening factors and supply constraints, but as #SupplyChains normalize from Covid-related shocks and #inventories rebuild, we expect much of the recent inflation will be transitory, with some stickiness in pricing pressure longer-run.

That may be especially the case where #inventory levels are harder to build up quickly and continued #demand from higher levels of #growth persist for at least the next year, or so.

With respect to today’s #inflation data, #coreCPI (ex. volatile food and energy components) came in strongly at 0.9% m-o-m and 4.5% y-o-y, above the consensus forecast and again driven higher by used vehicle prices, which rose by 10.5% on the month to hit a 45% gain y-o-y.

In our view, the question of #inflation’s “stickiness” will ultimately depend on the elasticity of supply for goods and services, but in the long run the aggregate #SupplyCurve has been extremely flexible and dynamic, even for #labor.

Hence, we believe it is hard to see a case for the current levels of elevated #inflation turning into “1970s style” runaway #price increases, but where does today’s data leave the #Fed’s policy reaction function?

We’ve argued that policy adjustments that are intentionally late, as the #Fed’s #AverageInflationTargeting goals may end up being, can create distortions in the #economy and #markets that (ironically) risk undermining the very successes that policy has achieved.

Therefore, we think the #Fed should adjust #MonetaryPolicy away from emergency conditions, as this is now distorting the economy and markets, particularly in #housing.

Indeed, purchasing $40 billion a month of Agency #mortgages at inflated prices only continues to overheat a #housing market that is beset by extremely low inventory and consequently surging prices (lower levels of #affordability).

• • •

Missing some Tweet in this thread? You can try to

force a refresh