The #economy and #markets today present us with a type of confusing environment: a tremendous growth rebound amid concerns over different forms of #overheating due to policy being late to normalize, and then the uncertainty of an ultimately harsher policy unwind down the road…

… It’s in this kind of environment that we find that what #investors want to do can be very different from what they need to do – the opposite, or mirror image, in fact: bit.ly/3u0nmr9

Over the last decade, the Bloomberg Barclays U.S. High Yield Index has traded in a #yield range of about 4% to 12%, and both those extremes have come during the pandemic period (the last 14 months).

At a 4% #yield, an #investor may want to own no high yield at all, but they may need to, in order to meet obligations and return targets: we’re blown away by how investors’ needs have dominated #markets, against our fears that prices are too high amid surging policy #liquidity.

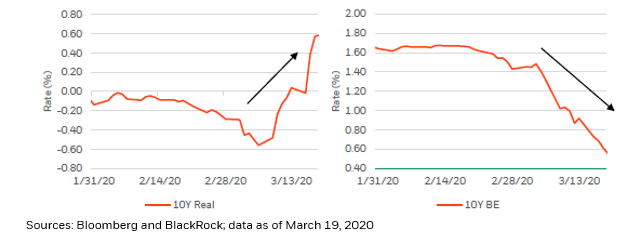

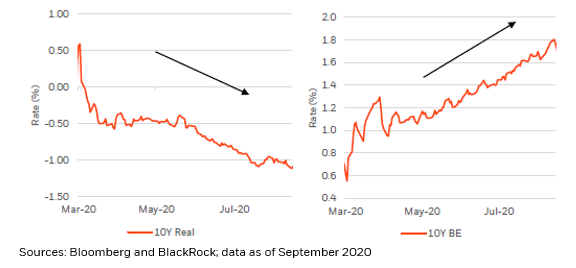

What #market participants want and need to do is to protect the purchasing power of their #capital – but that has never been more difficult, as capital in search of a positive real #yield (adjusted for #inflation) is being forced into a shrinking pool of assets.

Recently, we saw the first time that BBB-rated #CorporateBonds did not offer a positive real #yield, in data going back to at least 2002, while BB-rated #bonds (a subset of high yield) only barely make that cut…

Now, one has to go to the bottom of the #capital stack (to #equities) to find a positive real yield greater than 2% – and equity #earnings are somewhat “inflation hedged,” given companies’ ability to manage selling prices/costs…

… thus, #equities have a reasonable margin of safety against the #market’s expectations of future #inflation.

So, while we wait on the #Fed, and actually because the Fed is moving slowly, #technical factors may dominate #financial markets in the near term.

.#Investors are likely to continue to be forced to address their needs rather than their wants, while their #capital bases grow at a torrid pace, fueled by ongoing #liquidity injections.

• • •

Missing some Tweet in this thread? You can try to

force a refresh