,

29 tweets,

7 min read

Read on Twitter

Wrote some initial thoughts on what $FB Calibra wallet can bring to the payments landscape. TLDR; Facebook has positioned Calibra to benefit off a new design landscape for developers and businesses to come in and build value added fintech services on top-of Libra. A thread:

1/ We've seen this playbook before from Facebook via their Credits product, which launched its alpha almost a decade ago to the date. Media ate it up, buying into Facebook's projections that the virtual currency business system could one day be a "multi-billion dollar business"

2/ Spoiler alert: it didn't 'rule the world' and challenge payment businesses like CEOs originally feared. One of the core problems with the product was FB had to give back a majority of revenue to cover payment processing fees - an issue for micro-payments

3/ But that different time optically for FB, and a similarity between the two initiatives stops at the desire for lower-cost payments. In fairness to the Libra association, the ambitions of these projects are much grander than the ability to buy items for your Farmville plot

4/ The Founding Members bring serious strategic benefit to bootstrapping this network globally. Whether the $10 million entrance fee to have skin in the network (members will receive Libra to use to incentivize adoption) is enough to drive merchant acceptance remains to be seen

5/ At the very least not hard to imagine a16z and USV will push Libra within their portfolio companies where applicable. On the payments side, members exploring servicing opportunities either via on-ramps or on the processing side seems reasonbale. PayPal seems most likely here

6/ Uber and Lyft appear to have the most to gain from a lower-cost payment play within the group, given how large an impact card processing fees are on the business. Uber last year had +$43 billion worth of card volume processed, likely translates to > $1B in card processing fees

7/ The low-hanging fruit of a remittance play makes sense. According to the World Bank, in 1Q19 the global avg cost to send $200 was ~7% (banks ~11%). Interesting to see Western Union open down 3% yesterday (still down 2% as of post)...

8/ However, 2 headwinds on remitt op: estimated that 80% of market still done in cash, and Calibra wallet wont be available where crypto is banned by regulators. 2018's top2 remittance recipient corridors, India ($79B) and China ($67B), would be blocked off from Calibra’s rails

9/Another opportunity set that jumps out from the Calibra announcement is the ability for Facebook to boost digital wallet adoption both in the US market and abroad

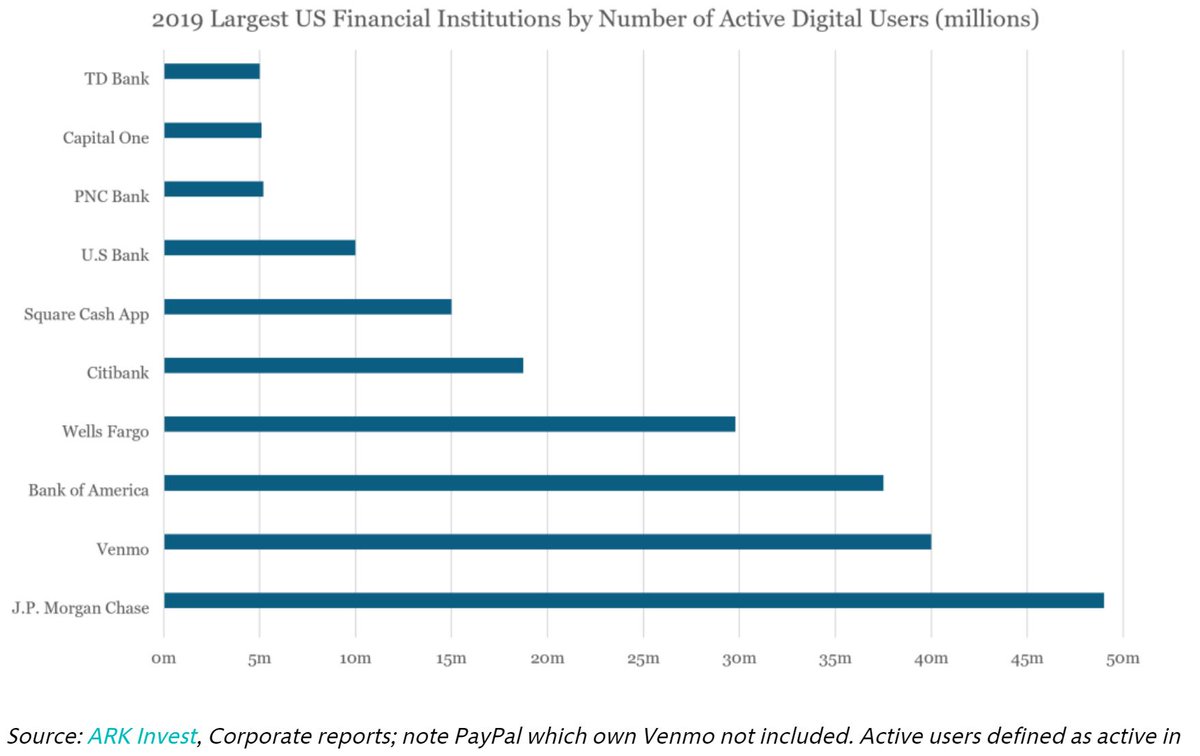

10/ Assuming a U.S. active user base of ~170m people, a 5% penetration rate in 2020 would put Calibra at #7 largest by active digital users, right behind Cash App. Open that 5% penetration to its ~2.3 billion monthly active global user base and its over 110m wallet accounts

11/ As for product offerings within the Calibra wallet, the announcement gives examples of feature-sets that could be built on top of the payment wallet, including lending, portfolio management tools (PFMs), QR purchases, and even contactless payment solutions for metro cards

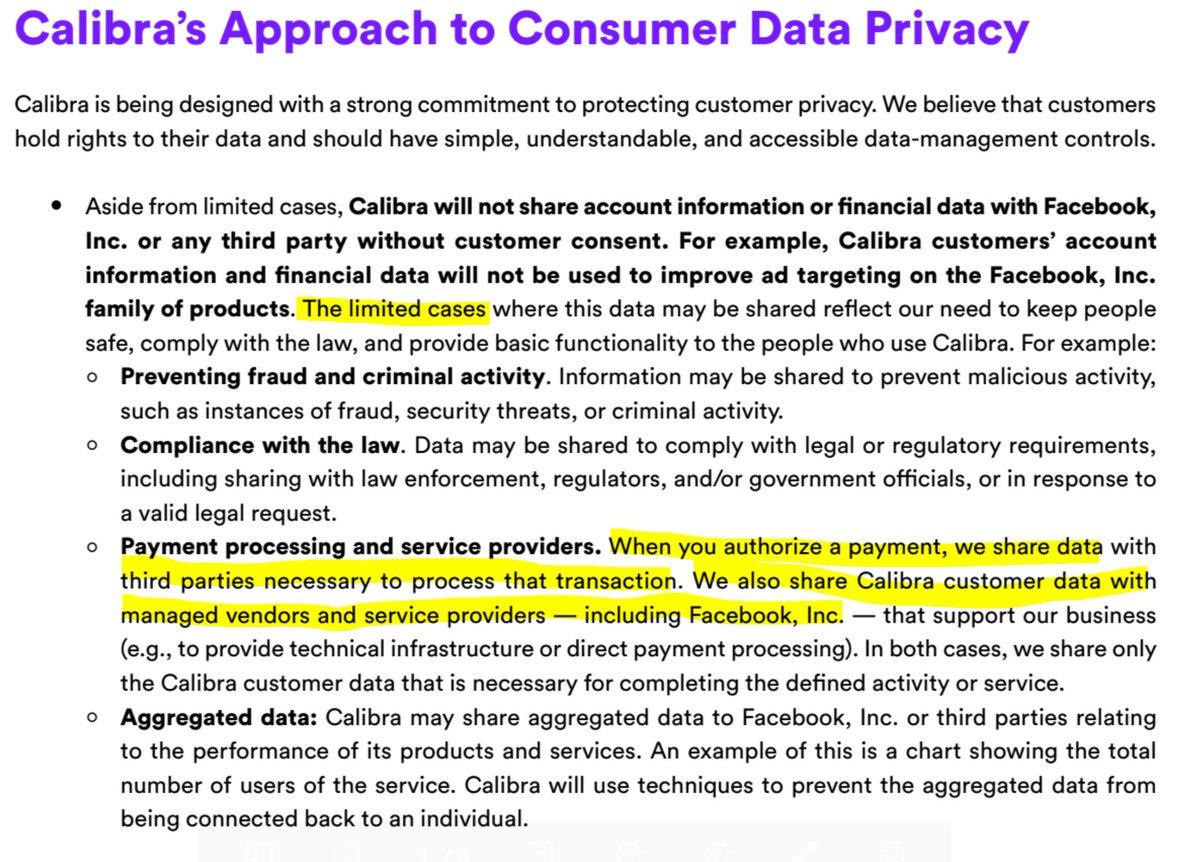

12/ What’s interesting about these examples is the hint that the wallet could have access to Level 3 transactional level data, or visibility into not just where and how much you purchased, but also an itemized receipt of the items that you purchased at a specific merchant...

13/ ...assuming the merchant uses Calibra or a connected processing service. This data policy note for Calibra also suggests as much. Payment processors and other services receives data when the user sends a payment

14/ To be clear, FB hasn’t confirmed this is the case or intention for Calibra to leverage this level of data. However, it’s not a stretch to think Calibra will look to offer value-added digital wallet services that consumer can opt-in for, even if it means giving access to data

15/ Some of these services could be personal finance tools, smart coupons and discounts, and even ad-driven rewards that send a small amount of Libra to your wallet after watching (see a16z video: the future of the mobile wallet for context)

16/ Curious to see businesses look to build on top of Libra, and whether they're crypto-native, consortium members, or mix of both. FB told The Block that it “looks forward to making Calibra interoperable with other apps and finserv providers that offer complementary services.”

17/ One clear opportunity I see is for lenders to explore the ecosystem, whether that’s integrating directly into Calibra or another Libra wallet, and either offer loans at the PoS, or just facilitate loans denominated in Libra. Great opportunity to explore micro-financing in EM

18/ @TheRealBlockFi, a crypto lending CO, told The Block it's bullish on asset backed stablecoin lending, and “would look to support Libra as an asset you can earn interest on, as loan disbursement mechanism, and accepted collateral for crypto loans.”

19/ To that end, this could be the nail in the coffin on DeFi lending providing "low-cost" consumer financing. Will we see some of these teams look to build on Libra instead? I've written about why DeFi lending doesn't solve financial inclusion here: theblockcrypto.com/2019/03/04/the…

20/ What's cool about the Calibra opportunities is that all of this is fair game for other COs. FB told The Block: “Any consumer, developer, or business can use the Libra network, build products on top of it, and add value through their services...

21/ ..."In fact, we welcome additional wallets that will provide consumers with choice and good competition that will benefit customers."

22/ Now all of this assumes that Libra actually gets cleared by regulators globally (a pretty big IF). Other questions I still have outside of regulatory concerns:

23/ Will this actually be THAT much cheaper than V/MA rails? Payments are already low-cost, you pay for value-added services like rewards, insurance, chargebacks for fraud, etc. Encouraging service providers to come build and help with on/off ramp implies fees across the stack

24/ How will the association fund rewards post-the initial Libra incentive pool being used up? Will a portion of the interest on reserves be used perpetually? Will that be enough? If not, the system could use transaction fees to fuel rewards but again that increases the costs

25/How will the payments Founding Members look to integrate this into their capabilities? How will big tech respond? Will there be a second consortium formed with different members (similar to Visa's consortium in response to Masterchange?)

26/ Other interesting thing to note. I've spoken to a # of sell-side analysts about Libra. Bifurcation is forming where internet teams view as something new and + to point to for FB, while pmts largely shrugging it off. Has got some realizing they need beef up on crypto knowledge

27/ Phew. If you made it this far and want to read the full piece:

theblockcrypto.com/2019/06/18/fac…

theblockcrypto.com/2019/06/18/fac…

Fin/ This research was part of @TheBlock__ Genesis previews where we share research that our subscribing members receive daily. If you or your team is interested in staying up to speed on this market, consider trying us out:

theblockcrypto.com/genesis/

theblockcrypto.com/genesis/