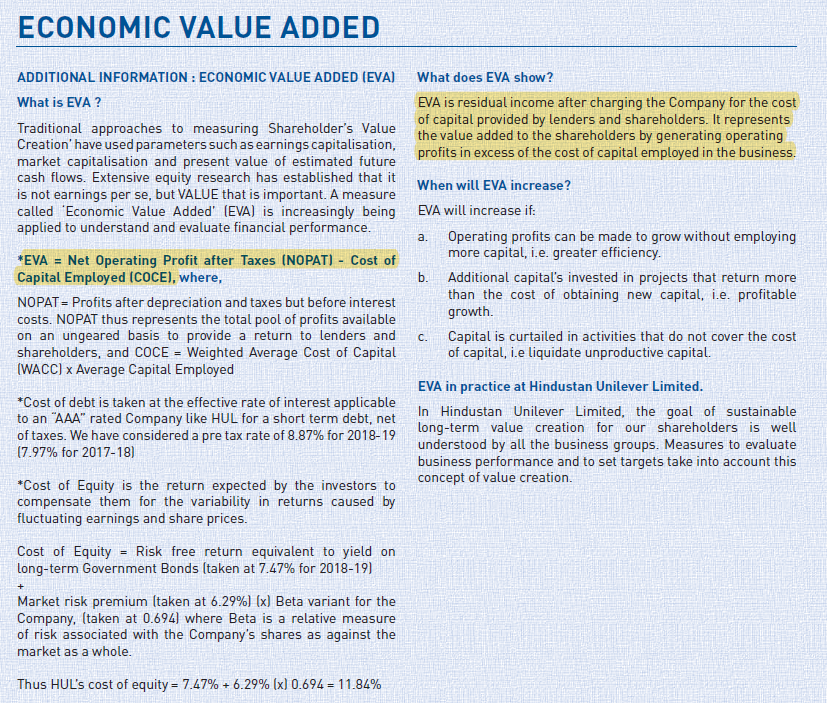

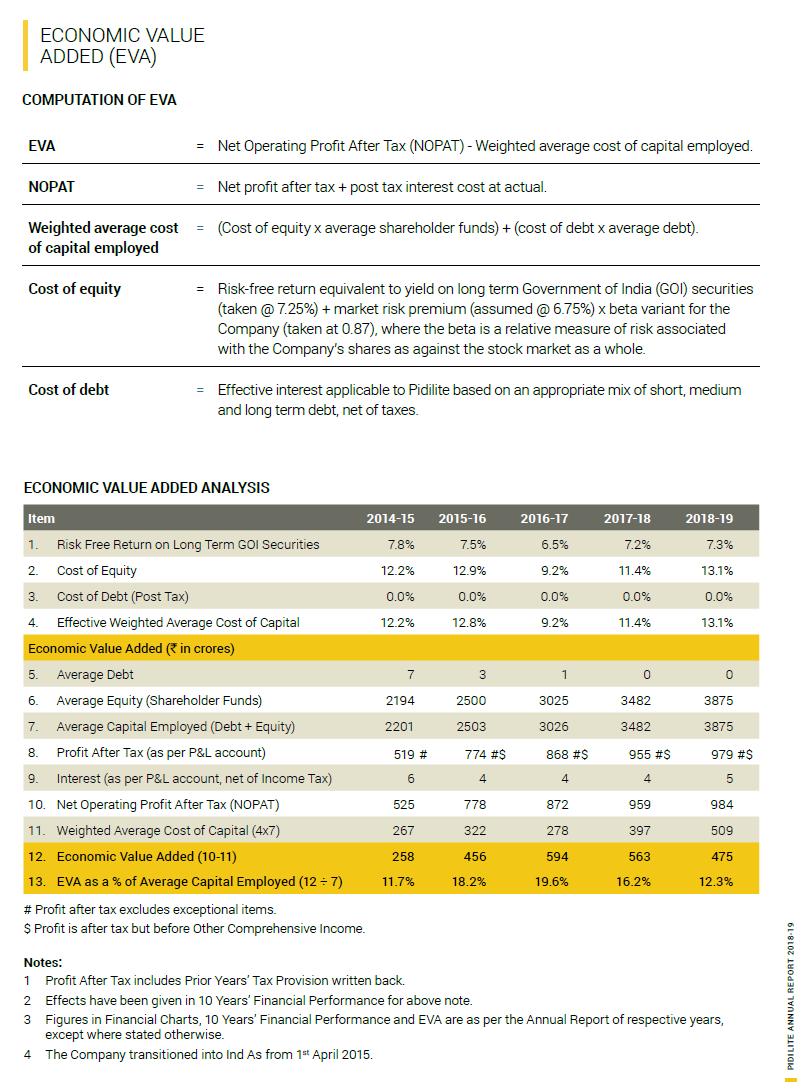

,

10 tweets,

4 min read

Read on Twitter

Recent Ambit report suggests a bearish outlook and that any 'turnaround' is distant. Sharing some data points below that merits broader dissemination. 👇

1/n

1/n

1. India's corporate profits to GDP ratio has been falling for a decade with profit and wage growth being at mutli-year lows. From being ~6% of GDP in 2008-09, we are down to ~2.5%. Comparisons with 2009 recovery may be wrong.

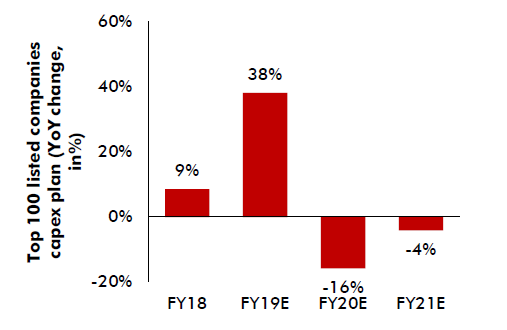

2. Capex revival has taken a u-turn. Top 100 companies have decided to pull back on investments in FY20 and FY21, an important leading indicator. Also, Central government capex is set to contract by 1% in FY20 vs 10% growth in FY19.

3. The above is a function of sub-optimal capacity utilization, which is linked to lower than anticipated domestic demand. 11 of 13 major sectors in India currently have utilisation levels below 80%. However, system wide utilization is has marginally improved from 72% to 76%.

4. Export opportunity that opened from US-China tariff wars in moving away due to increasing import tariffs in India. With global trade restrictions at multiyear highs, export to remain muted. India has one of the highest import tariffs globally in F&B, Auto & Industrial supplies

5. The rural growth story is past its peak. Agri's share in GDP is falling faster than share in employment, indicating lower productivity. Rural growth over FY04-15 was driven by UPA's 'fiscal largesse'/ populist measures + upswing in food prices. Demon has hit rural segment hard

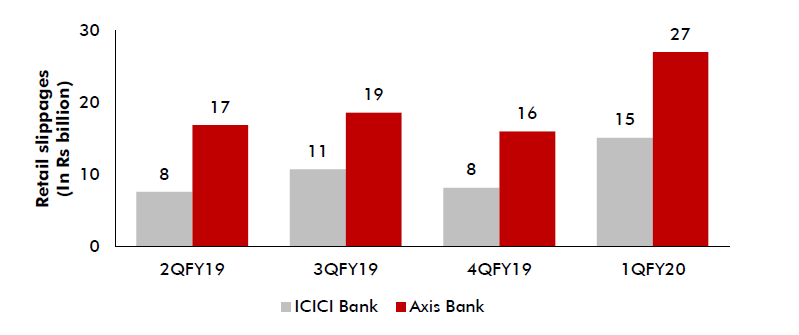

6. Early warning signs that "source of credit stress" is spreading beyond sectors like Infra to retail and SME. Retail slippages for large private banks have increased in Q1F20. Aligns with points raised in this coverage:

economictimes.indiatimes.com/industry/banki…

economictimes.indiatimes.com/industry/banki…

7. Slowdown in investment ecosystem is visible in reducing deal-activity across PE/VC space in the last one year.

8. As against popular views, markets are not cheap compared to historical averages. Nifty 50, 100 and 500 components still trading at a premium to 5 year, 7 year and 10 year avg P/E rations. (refer Point 1 on declining corp profitability to GDP).

9. Investment implications:

a. Both consumption & investment growth to remain muted in FY20.

b. Suggests an "extremely defensive strategy"

c. Sell on "high end" & "rural consumption" plays

d. Buy on "low and mid-ticket consumption plays"

e. +ive on Corp focused Banks & Insurance

a. Both consumption & investment growth to remain muted in FY20.

b. Suggests an "extremely defensive strategy"

c. Sell on "high end" & "rural consumption" plays

d. Buy on "low and mid-ticket consumption plays"

e. +ive on Corp focused Banks & Insurance