,

21 tweets,

5 min read

Read on Twitter

Great primer on negative bond yields. Thread! There are a couple types of interest rates that can be negative. The ones that we are most interested in are 1) interest on reserves and 2) (market) yields on government and corporate bonds. 1/

For the first type: Interest on reserves relates to monetary policy by central banks (Fed, ECB, Bank of Japan). Every day, commercial banks in these countries have to decide what to do with the cash they hold on their balance sheets. 2/

Commercial banks are required to hold a certain amount of cash (required reserves) on their balance sheets at all times. The amount each bank must hold depends on the size and nature of that bank's liabilities. Some central banks pay interest on these reserves. 3/

The amount banks hold over and above the required reserves is called "excess reserves." Many central banks pay interest on these reserves as well. The Fed (US) pays 2.10%/yr on both required and excess. By contrast, the ECB pays -0.40%/yr on excess reserves! 4/

Why? The ECB is trying to stimulate the economy, so it penalizes banks that have cash that they are not lending to businesses, etc. For these banks, they are forced to PAY the ECB 0.40%/yr on cash that they hold in excess reserves. 5/

In theory, this will simulate the economy by forcing banks to make loans. Is it working? There's a fair amount of evidence that it might not be, but this is beyond the scope of my thread. 6/ reuters.com/article/us-ecb…

These central bank rates are what we call "nominal" negative rates, meaning that the actual/stated rate the central bank is paying/charging is actually negative (banks have to write a check to the ECB for the privilege of holding cash there). 7/

Japan and many other countries have had nominal negative reserve rates on and off for many years. 8/ nytimes.com/2016/09/21/bus…

The second type of negative interest rate is probably more interesting, complex, and harder to understand. This second type of negative interest rate is called a "market rate" or a "yield to maturity." 9/

This yield to maturity (YTM) is the expected rate of return that an investor will receive when buying a bond. IT DOES NOT MEAN that governments and corporations are issuing debt that requires the investor write a periodic interest check to the government or corporation. 10/

The rate that the bond promises to pay the investor is called the coupon rate (or stated or nominal rate). The rate that the investor actually earns on holding the bond is the YTM. 11/

Example: A 2-year bond is issued today with a 3% annual coupon rate. Investor pays $100 (par value) today. Investor receives interest each year of $3 (.03 x 100). At the end of year 2, he gets back his par value of $100. This bond has a coupon of 3%/yr and a YTM of 3%/yr. 12/

Same bond, but instead of paying $100 for the bond, the investor pays $106 (this is a premium to the par value). He receives $3 each year and $100 at the end. This bond has a coupon of 3%/yr & a YTM of 0%/yr. (investor got a total of $106 in cash flows that he paid $106 for). 13/

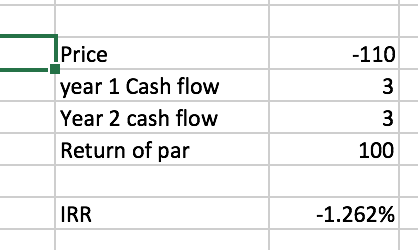

Same bond, but instead of paying $100 for the bond, the investor pays $110 (this is a premium to par value). He receives $3 each year and $100 at the end. This bond has a coupon of 3% but an (annual) YTM of -1.26% (investor got $4 less in cash flows than he paid for) 14/

(Math for 14/ above involves solving for the internal rate of return for the cash flows described, which takes into account present value of the payments, but the intuition should be clear without the math) 15/

The situation is 14/ is pretty rare (it is quite rare for a company to issue a new bond at a premium/price that implies a negative YTM, although it can happen). 16/ global-macro-monitor.com/2019/08/08/neg…

But, it is increasingly common worldwide for bonds that are already issued and trading on the open market to have this situation happen. So to extend the example above, it could be the case that a company issued a bond at $100, with an expected YTM of 3% (12/ above) 17/

Over time, as the bond trades on the open market, the price of the bond rises to $110. (WHY? See next tweet). The investor who bought the bond at issue price of $100 can sell it to a new guy for $110. The new investor has expected YTM of -1.26%. The first investor makes bank. 18/

Why would the price rise so much? The article does a good job here: investors are nervous, so they want to buy safe bonds like German bunds, etc. They are willing to accept negative expected YTMs in return for perceived safety. 19/

So, to wrap up. Negative nominal rates *generally* only exist in the central bank world. 20/

Negative YTMs mostly exist in the trading world, and mainly on the secondary market. This occurs when bond prices are so high that the expected coupon payments for the bond are insufficient to cover the high price paid for the bond. 21/21.