,

17 tweets,

19 min read

Read on Twitter

1) On 25 July, Tribeca's Commodity Trading Specialist Guy Keller gave an excellent presentation outlining their #bullish #Investment case for #Uranium, expecting to increase their exposure to #U3O8 sector over rest of 2019 as #nuclear demand grows... asx.com.au/asxpdf/2019072…

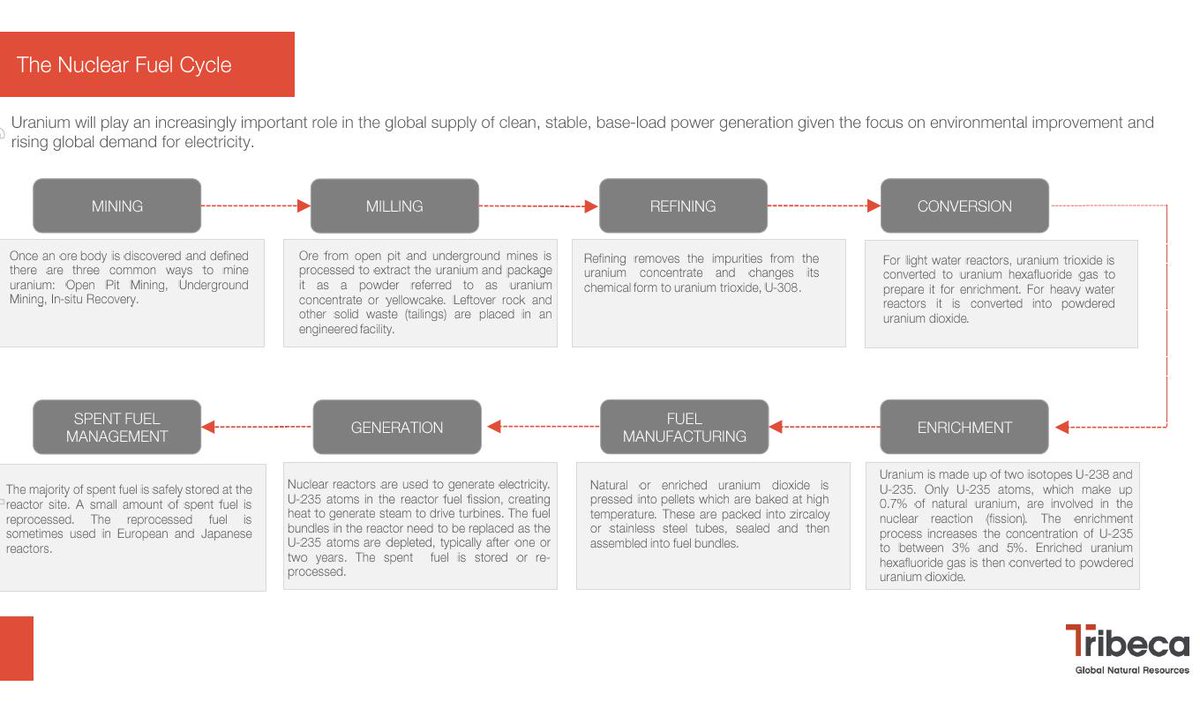

3) #Uranium will play an increasingly important role in global supply of clean, stable, #nuclear base-load power generation given today's focus on environmental improvement amid rising global demand for #CarbonFree low emissions #electricity...

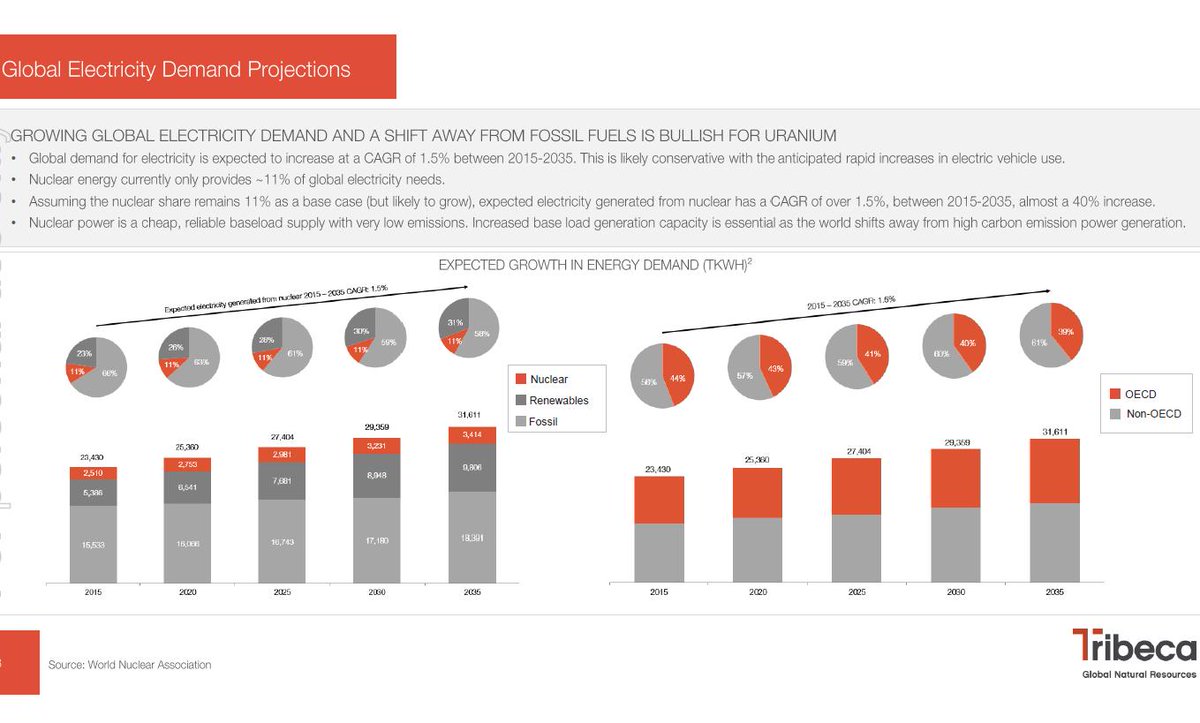

6) Global #Electricity demand is growing while power generation shifts away from carbon emitting fossil fuels, with ~40% growth in #nuclear #energy anticipated by 2035 in order to maintain nuclear's #CarbonFree cheap, reliable base-load supply at current 11% of electricity mix...

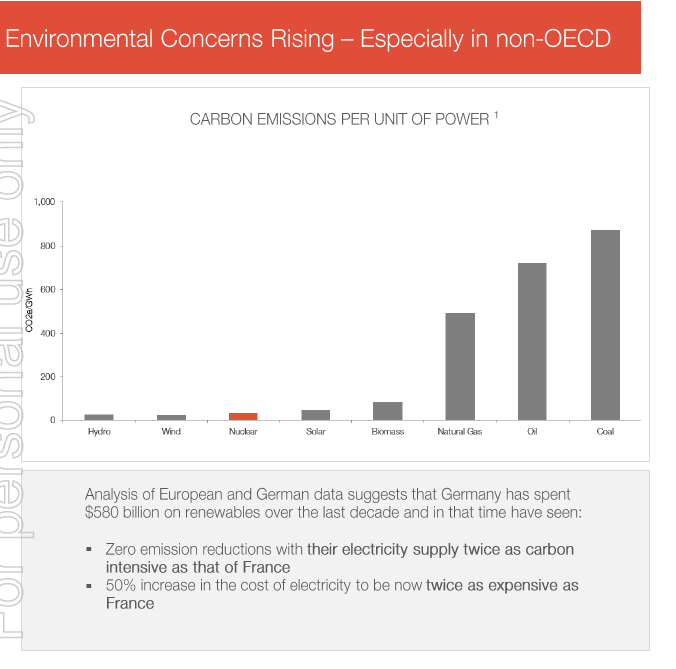

7) Environmental concerns rising on impacts of carbon emissions, especially in non-OECD nations. Failed experiment in #Germany shows $580B investment on #renewables saw NO REDUCTION in emissions (double those of #nuclear #France) & 50% rise in #electricity costs (2x $ France)...

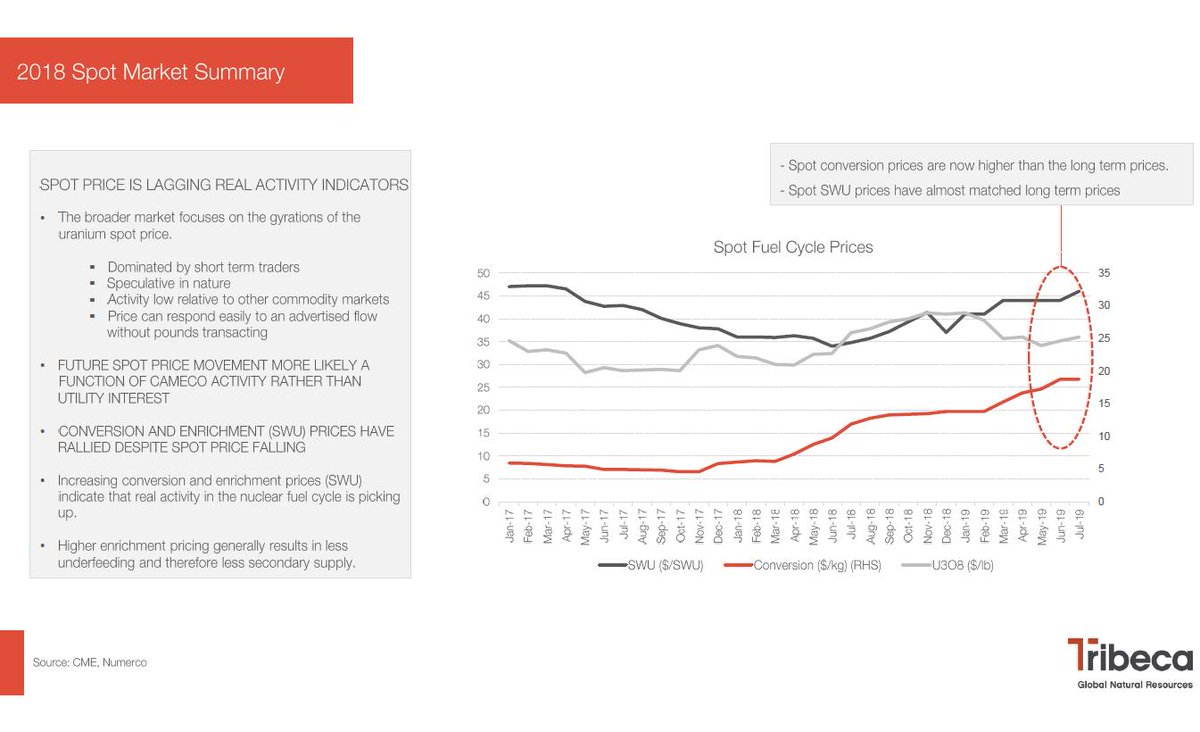

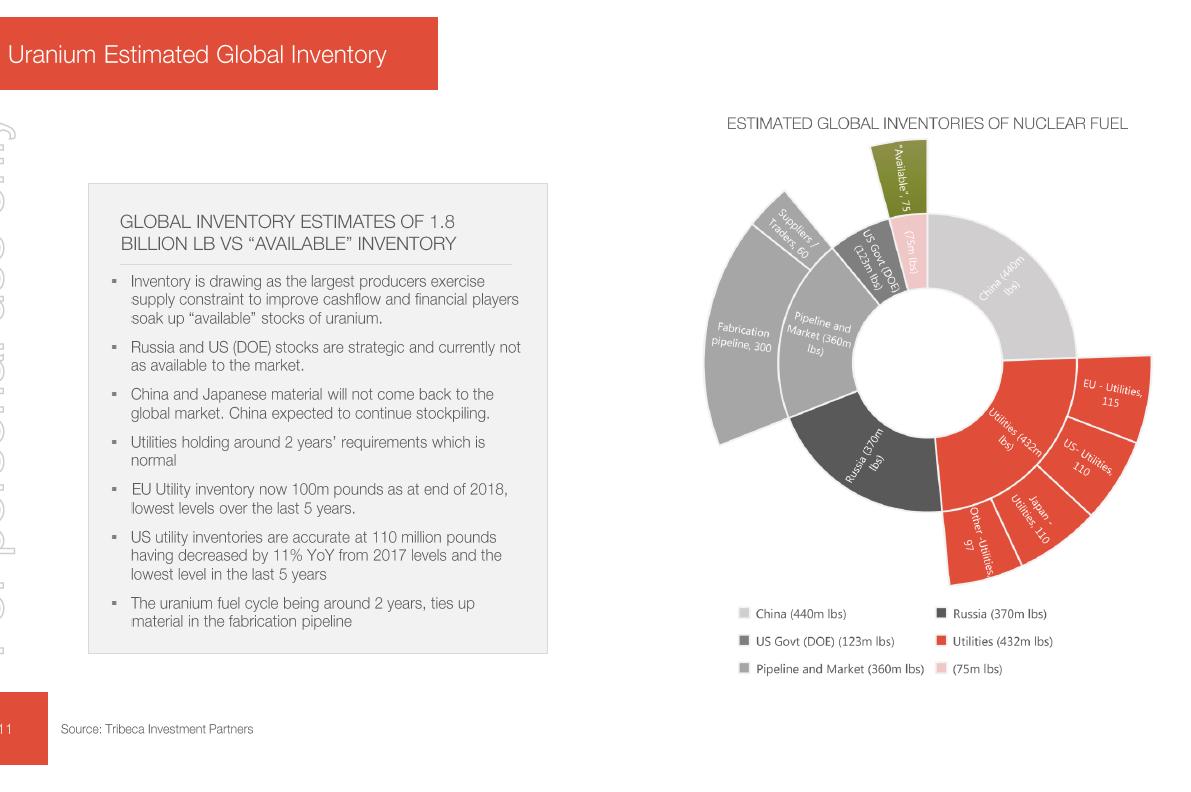

10) Classic mistake made by #investors is in analyzing #uranium global inventories. Only 75M lbs of estimated 1.8B lbs, less than 6 months #nuclear fuel demand, is actually "available". Inventories are at 5 year lows in EU & US while financial players "soak up" what's available..

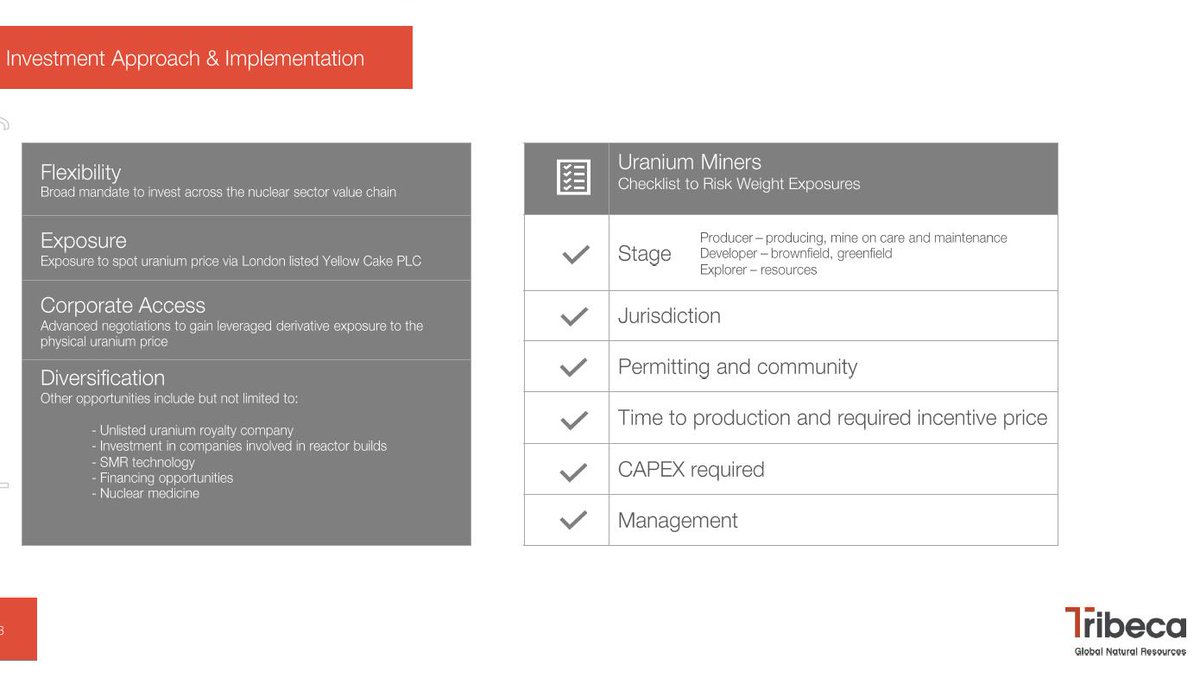

17) In conclusion, Tribeca provides their #investment approach for #uranium miners, and highlights Boss Resources (#ASX: $BOE) as Case Study that fits their #investing strategy. Sorry for the long thread but I felt it was worth the effort! #U3O8 Bull Market is emerging! 🐂🤠📈