🌎 The drag from global trade of goods (in volume) will be weaker in 2020.

➡ Based on CPB data, after (probably) contracting in 2019, global trade of goods (in volume) will grow again in 2020 ❗ (but at a slower pace than Global GDP)

➡ Based on CPB data, after (probably) contracting in 2019, global trade of goods (in volume) will grow again in 2020 ❗ (but at a slower pace than Global GDP)

🌎 Signs coming from the two leading sectors namely #semiconductors and #autos suggest that downward pressures will keep easing in the coming months.

🌎 It can be explained by several factors:

*Positive base effects

*Combined easing of monetary policy and trade tensions (especially U.S./China) for the first time in 7 quarters.

*Fiscal stimulus (China, Japan, South Korea, Germany, France, etc)

*Positive base effects

*Combined easing of monetary policy and trade tensions (especially U.S./China) for the first time in 7 quarters.

*Fiscal stimulus (China, Japan, South Korea, Germany, France, etc)

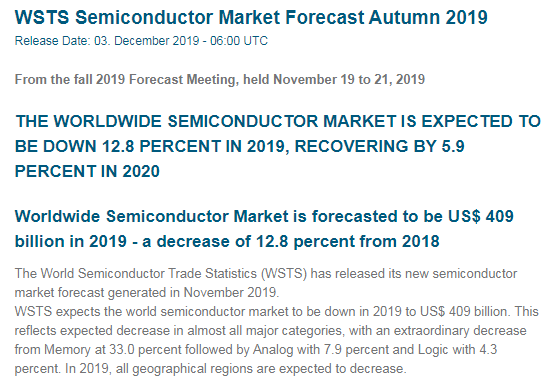

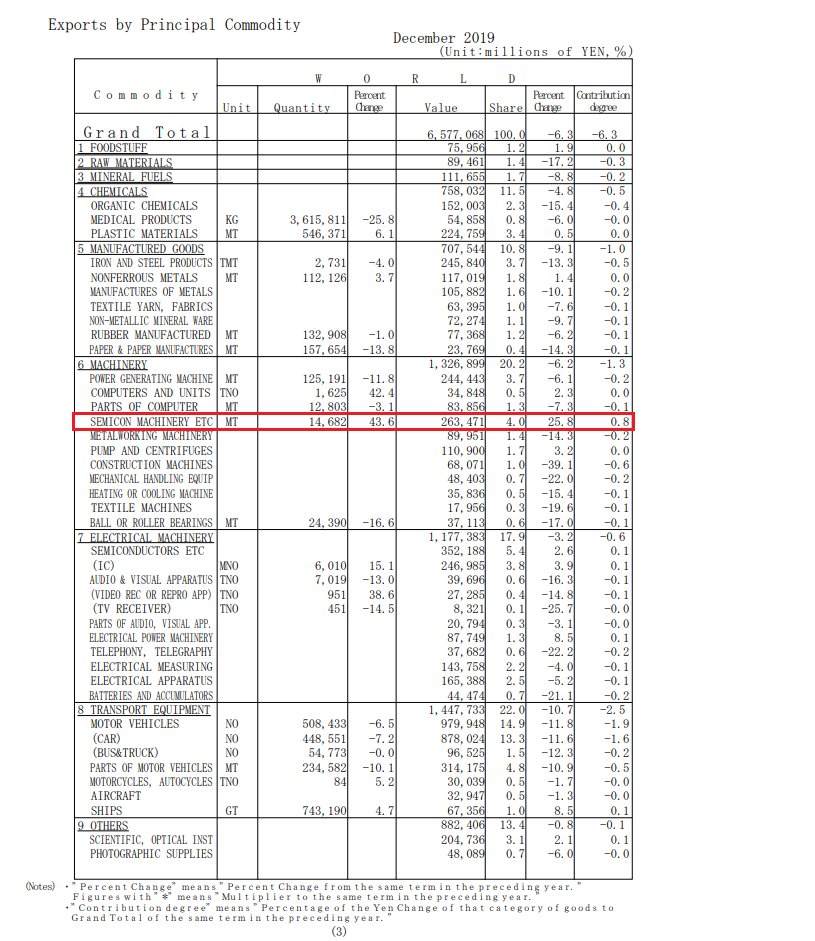

🌎 #Semiconductors (1)

*Worldwide sales (3-month moving average) fell 13.1% YoY In Oct. but it was the smallest drop since April 2019.

*Worldwide sales (3-month moving average) fell 13.1% YoY In Oct. but it was the smallest drop since April 2019.

🌎 #Semiconductors (2)

*In Oct., global sales ⬆ MoM for the fourth consecutive month (with my proxies suggesting that volumes are leading the charge)

*As a result, WSTS projects annual global sales will ⬆ by 5.9% in 2020 (v -12.8%e this year)

*Link: bit.ly/38q2lww

*In Oct., global sales ⬆ MoM for the fourth consecutive month (with my proxies suggesting that volumes are leading the charge)

*As a result, WSTS projects annual global sales will ⬆ by 5.9% in 2020 (v -12.8%e this year)

*Link: bit.ly/38q2lww

🌎 #Semiconductors (3)

*A rebound of global sales can also be explained by specific factors:

a/ The normalization of Intel CPU Supply Shortage will be positive

*A rebound of global sales can also be explained by specific factors:

a/ The normalization of Intel CPU Supply Shortage will be positive

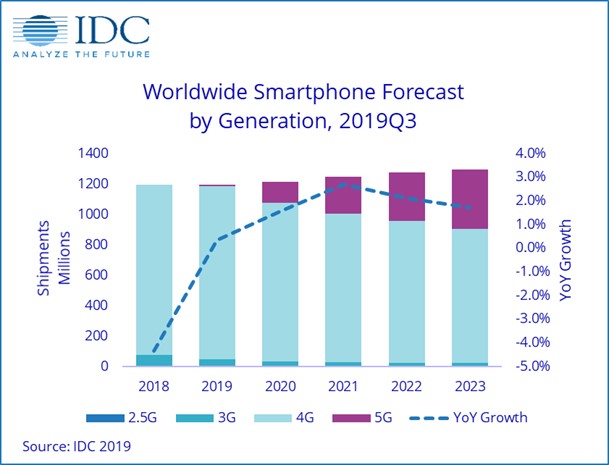

🌎 #Semiconductors (4)

b/ Global smartphone shipments are expected to grow in 2020 (+1.5%) after 3 consecutive years of market contraction, fueled by #5G plans in #China, according to the International Data Corporation (IDC).

*Link: bit.ly/36G0rGA

b/ Global smartphone shipments are expected to grow in 2020 (+1.5%) after 3 consecutive years of market contraction, fueled by #5G plans in #China, according to the International Data Corporation (IDC).

*Link: bit.ly/36G0rGA

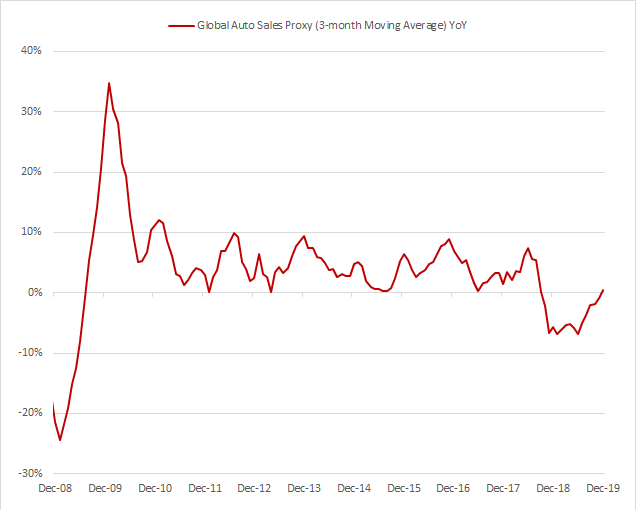

🌎 #Semiconductors (5)

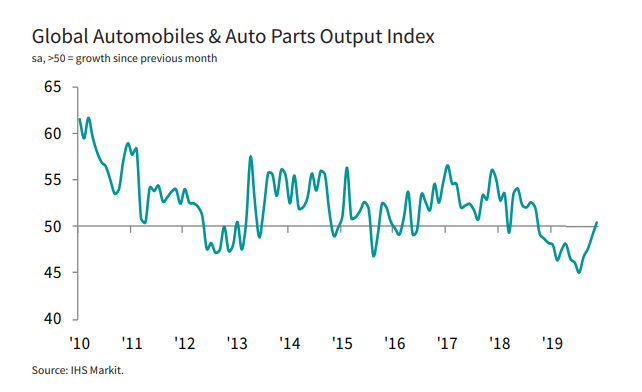

c/ Global auto production (~10% of the semiconductor market) should stabilize in 2020 as suggested by the first sign of recovery in Nov.

*According to Markit, global autos output ⬆ for the 1st time since Sep. 2018.

*Link: bit.ly/35qG93n

c/ Global auto production (~10% of the semiconductor market) should stabilize in 2020 as suggested by the first sign of recovery in Nov.

*According to Markit, global autos output ⬆ for the 1st time since Sep. 2018.

*Link: bit.ly/35qG93n

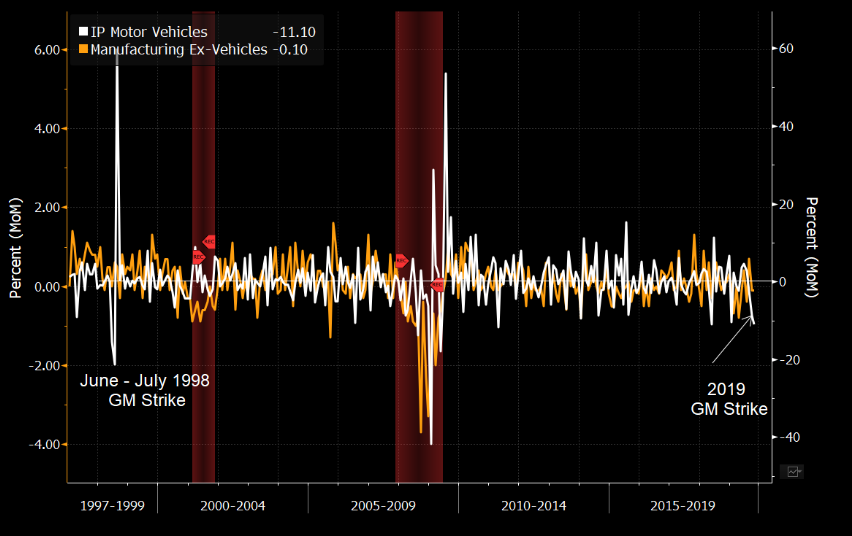

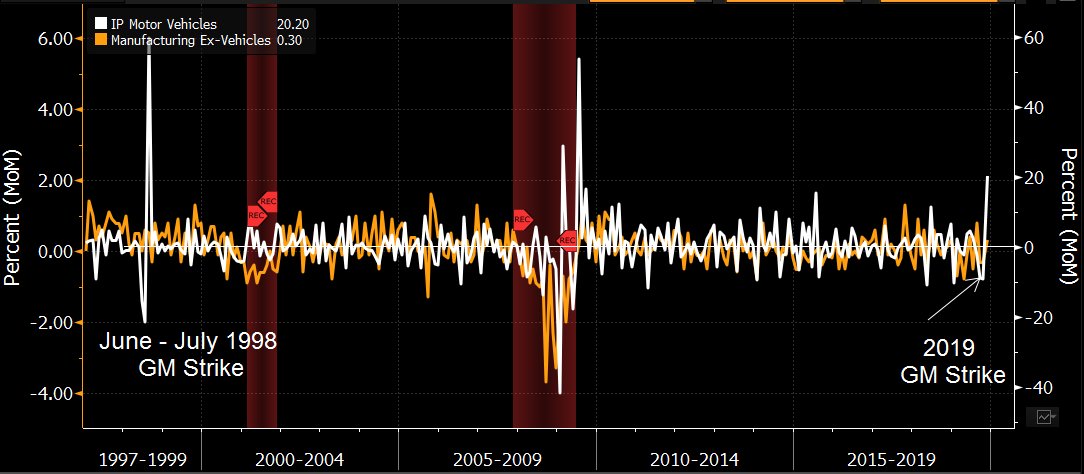

🌎 #Autos (2)

*Figures will also improve in the U.S. from Nov. following the end of GM strike (see 🇺🇸 figures this afternoon).

*Chart from BBG ⬇

*Figures will also improve in the U.S. from Nov. following the end of GM strike (see 🇺🇸 figures this afternoon).

*Chart from BBG ⬇

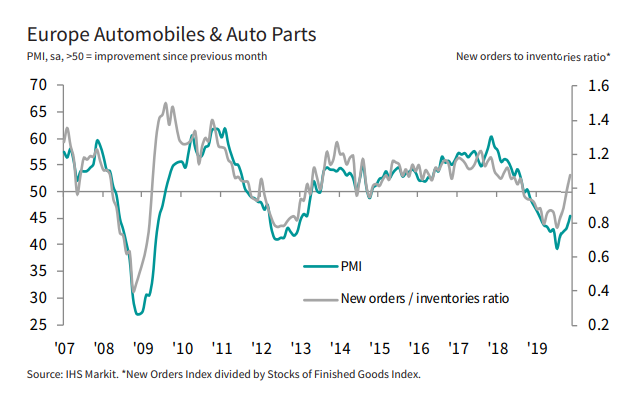

🌎 #Autos (3)

*Leading indicators suggest that auto sector in #Europe could recover in 1H20…

*Link (Markit): bit.ly/2YQO7jS

*Leading indicators suggest that auto sector in #Europe could recover in 1H20…

*Link (Markit): bit.ly/2YQO7jS

🌎 #Autos (4)

…while in Asia, “Automobile & Auto Parts producers already recorded a third successive rise in output that was the strongest since April.”

*Link (Markit): bit.ly/2Pq14y3

…while in Asia, “Automobile & Auto Parts producers already recorded a third successive rise in output that was the strongest since April.”

*Link (Markit): bit.ly/2Pq14y3

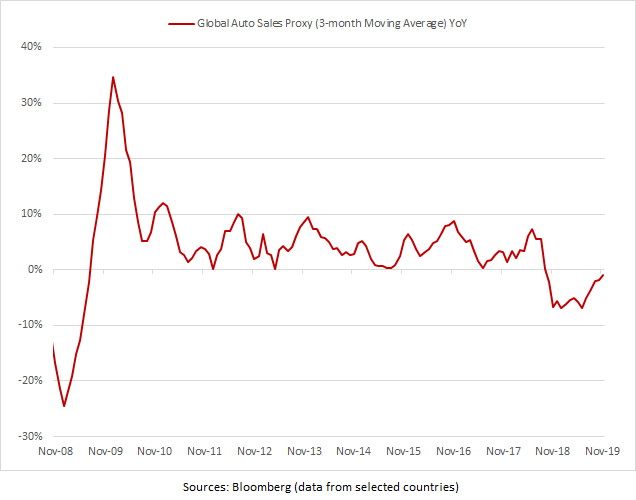

🌎 #Autos (5)

*My proxy confirm that, on YoY basis, global auto sales contracted at a weaker rate in late 2019.

*My proxy confirm that, on YoY basis, global auto sales contracted at a weaker rate in late 2019.

🇺🇸 As expected (bit.ly/36JtSHF), U.S. "Motor vehicles" production ⬆ 20.2% MoM in Nov., pushing the YoY rate to +1.5% (v -14.3% prior)

*Chart (updated) from BBG:

*Chart (updated) from BBG:

🌎 #Semiconductors | Micron Gives Strong Outlook, Suggesting Demand Is Rebounding - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

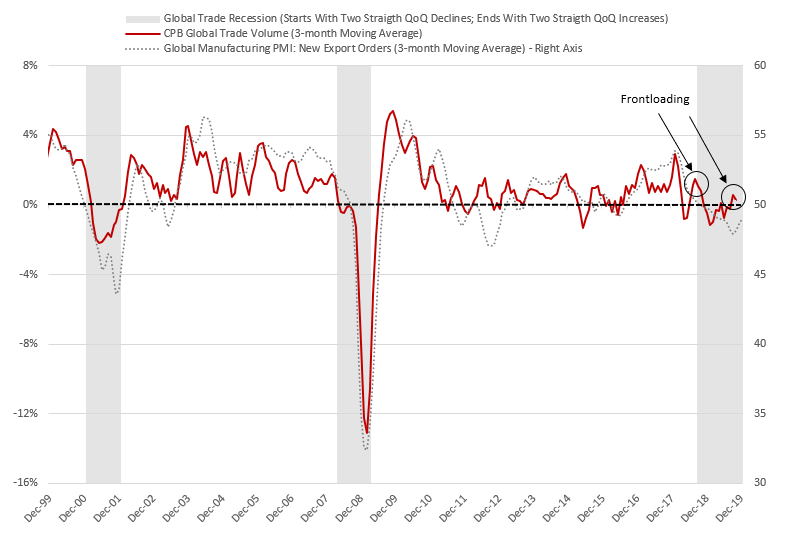

🌎 Another factor which suggests that, on a YoY basis, global trade growth (CPB data) should decline sharply in Oct. and then will recover the following months.

🇨🇳 #China | The list allows lower tariffs on goods coming from World Trade Organization members and will support trade flows from Jan. 1, 2020.

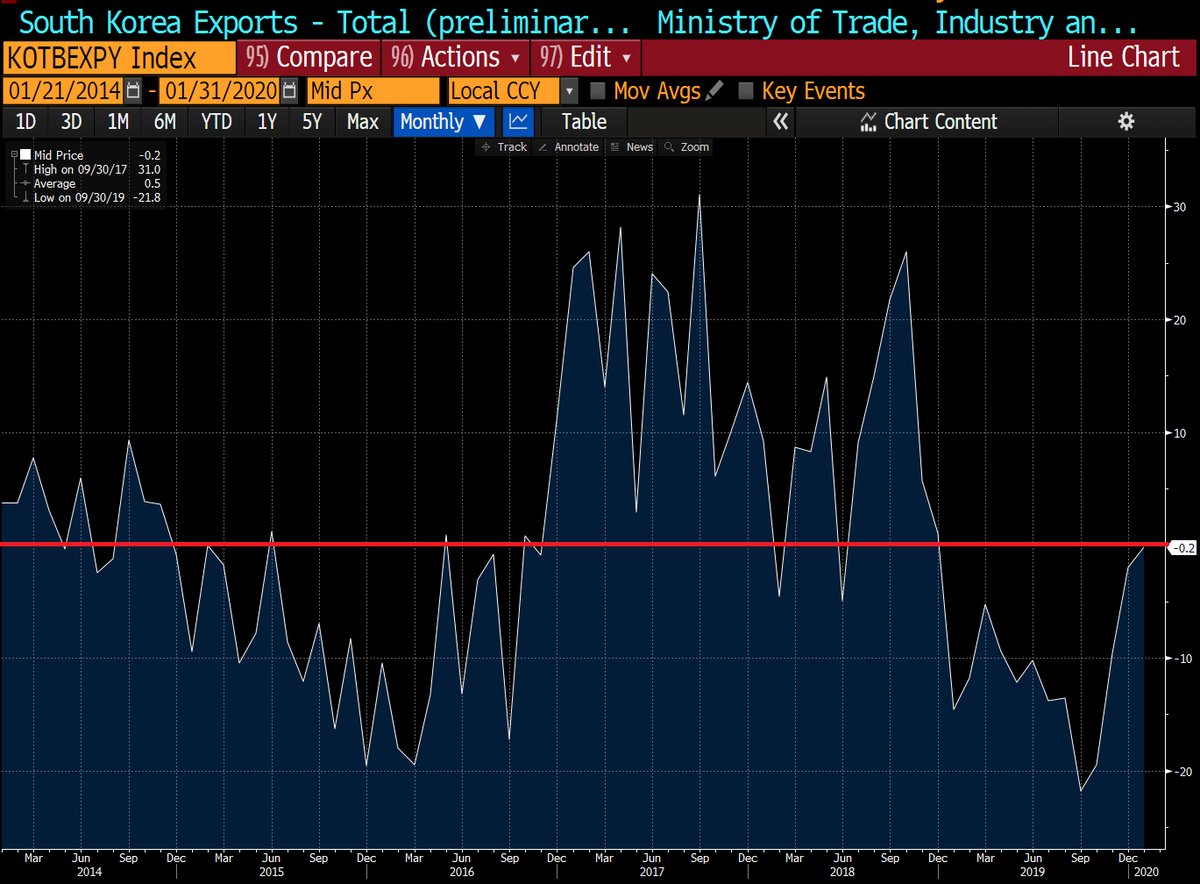

🇰🇷 #SouthKorea Dec 1-20 Exports Y/Y (0.5 more business days): -2.0% v -9.6% in Nov. 1-20

*Daily Average Y/Y: -5.1%❗ v -9.6% in Nov. 1-20

*Exports to #China Y/Y: +5.3% v -8.1% in Nov 1-20

*Semiconductor Exports Y/Y: -16.7% v -23.6% in Nov 1-20

*Link: customs.go.kr/kcshome/

*Daily Average Y/Y: -5.1%❗ v -9.6% in Nov. 1-20

*Exports to #China Y/Y: +5.3% v -8.1% in Nov 1-20

*Semiconductor Exports Y/Y: -16.7% v -23.6% in Nov 1-20

*Link: customs.go.kr/kcshome/

🇰🇷 Even if figures were boosted by a calendar effect, the daily average declined less than in October, confirming my view that #SouthKorea exports (global bellwether) will improve.

🌎 Summary: My Expectations Concerning Global Trade (CPB data)

1/ October: Expect a large decline YoY amid negative base effect (next release on Dec. 24th: bit.ly/2Sifylr)

1/ October: Expect a large decline YoY amid negative base effect (next release on Dec. 24th: bit.ly/2Sifylr)

2/ 4Q19: It should be negative again post frontloading in Q319.

3/ 2020: Flows should normalize upward mainly due to easing trade tensions and improvement in both #semiconductors and #autos.

🇺🇸 🇧🇷 #Trump Drops Threat to Levy #Tariffs on Brazilian #Steel and #Aluminum - WSJ

wsj.com/articles/trump…

wsj.com/articles/trump…

🌎As I already discussed (bit.ly/2PYc1r7), on a YoY basis, I think that October should be the bottom and then global trade growth will improve the following months.

🇨🇳 #China’s Economy Ends 2019 Brighter With Trade Deal in Sight - Bloomberg

*New export orders expand for first time since May 2018❗

*Link: bloom.bg/36aXDBf

*New export orders expand for first time since May 2018❗

*Link: bloom.bg/36aXDBf

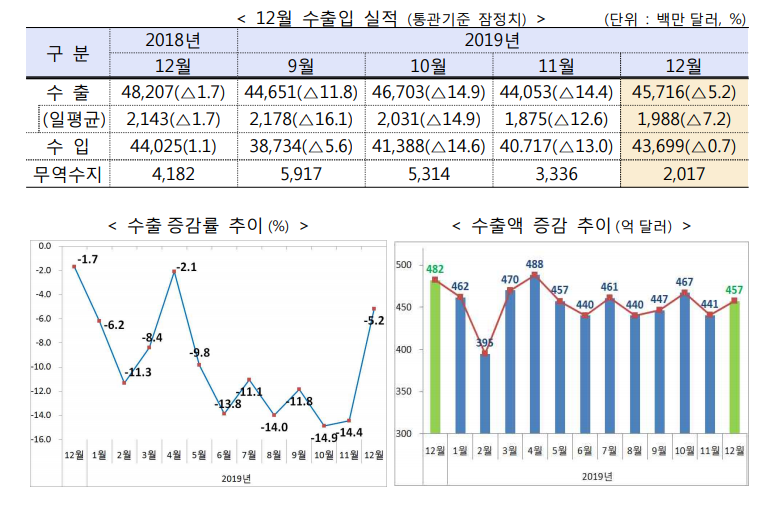

🇰🇷 #SouthKorea December Exports Y/Y: -5.2% v -14.4% prior (13th straight ⬇ but smallest ⬇ since April 2019❗)

*Exports Daily Average: -7.2% v -12.6% prior

*Exports to #China: +3.3% v -12.3% prior (first gain in 14 months)

*Link: bit.ly/33EQjMa

*Exports Daily Average: -7.2% v -12.6% prior

*Exports to #China: +3.3% v -12.3% prior (first gain in 14 months)

*Link: bit.ly/33EQjMa

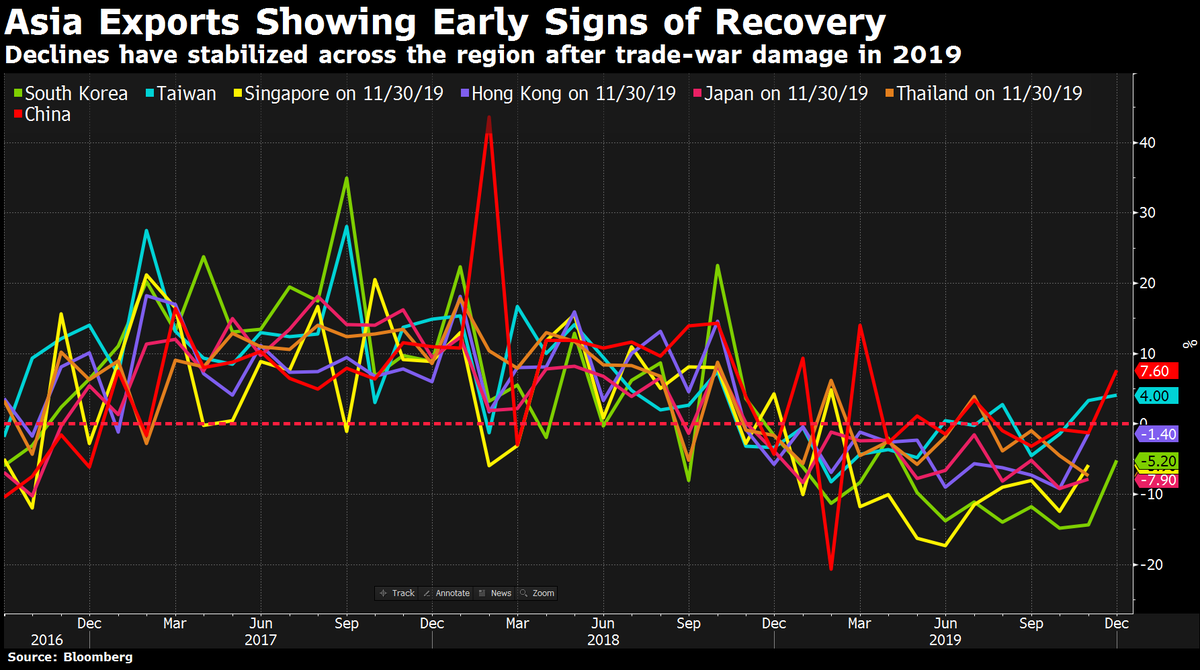

🌎 Dec. Global #Manufacturing PMI: New Export Orders: 49.2 v 48.9 prior (16th straigth contraction but highest since Jan. 2019)

➡ The 3-month average suggests that downward pressures on global trade growth (goods) may have bottomed but persisted in 4Q19.

➡ The 3-month average suggests that downward pressures on global trade growth (goods) may have bottomed but persisted in 4Q19.

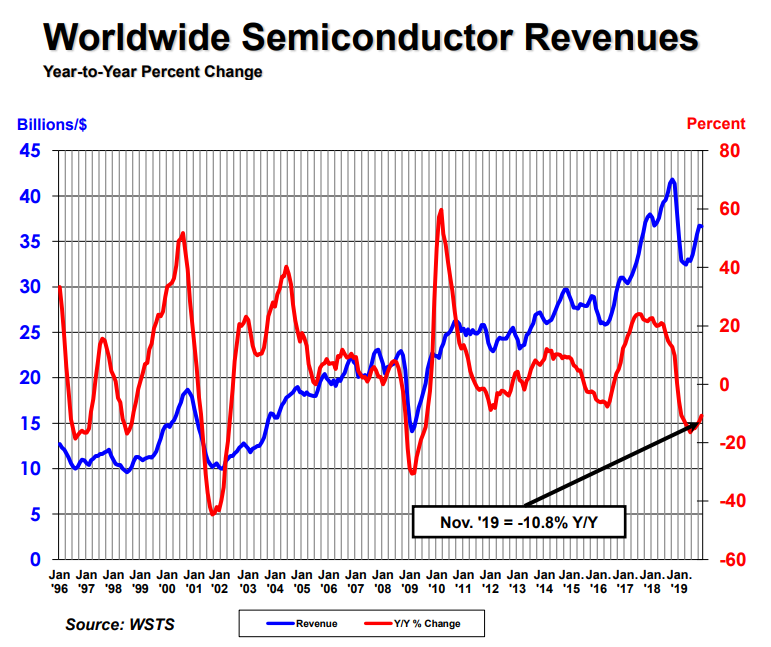

🌎 #Semiconductors | Worldwide sales (3-month moving average) fell 10.8% YoY In Nov. but it was the smallest drop since Feb. 2019).

*Link: bit.ly/2ZHHPDR

*Link: bit.ly/2ZHHPDR

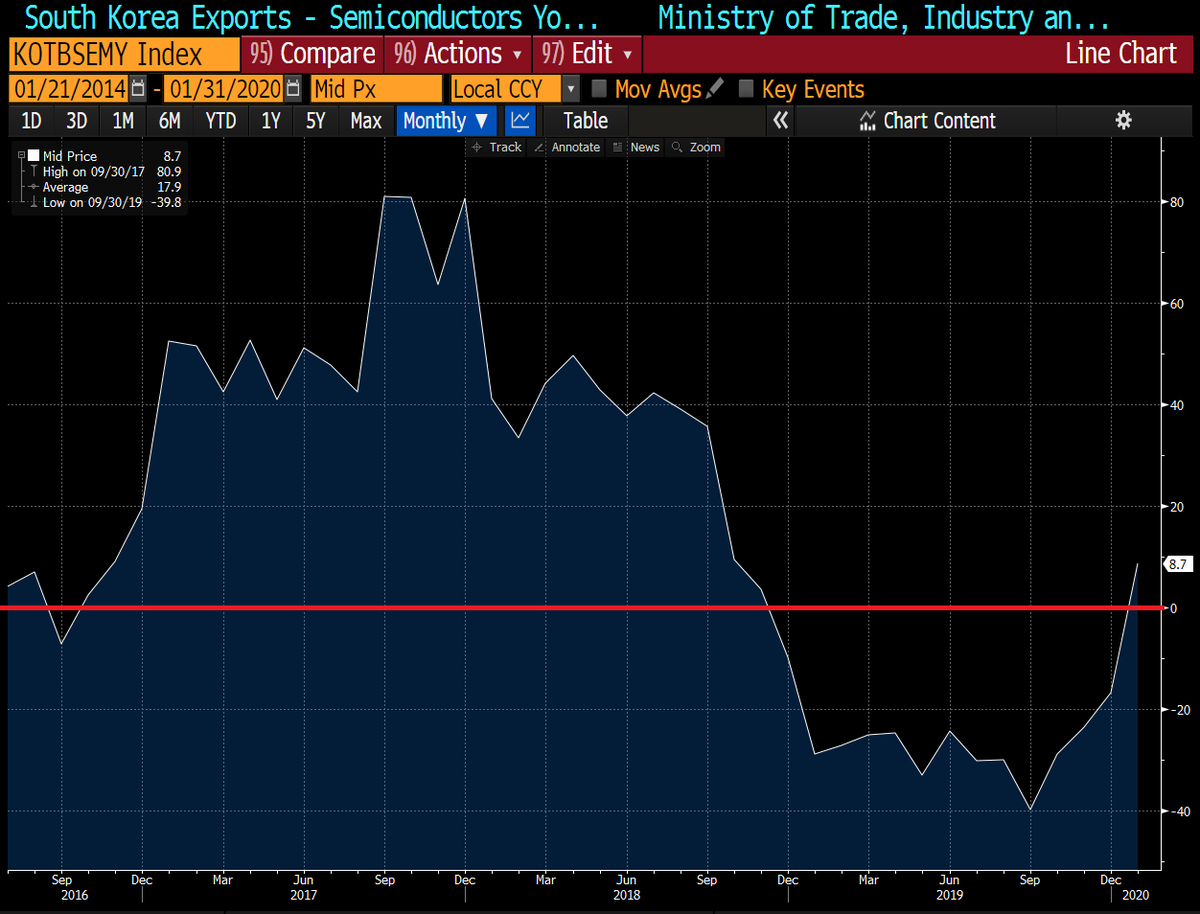

🇰🇷 #SouthKorea December #Semiconductors Exports Y/Y: -17.7% v -30.8% prior (13th straight ⬇ but smallest ⬇ since April 2019)

➡ It suggests that Global Billings should keep improving in December and confirms that worst is behind us.

➡ It suggests that Global Billings should keep improving in December and confirms that worst is behind us.

🇨🇳 🌎 #China-made exports of Ford, Tesla, BMW set to surge as Beijing opens auto industry, government says - SCMP

scmp.com/economy/china-…

scmp.com/economy/china-…

🌎 #Semiconductors | Samsung to Unveil New Devices Next Month in San Francisco - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

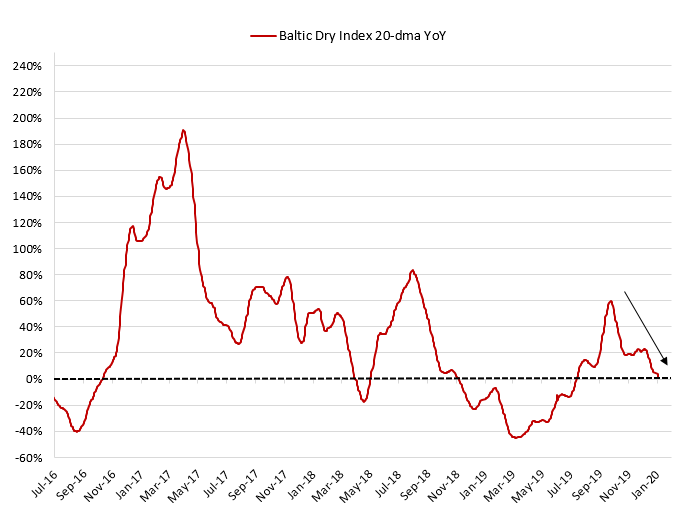

🌎 Baltic Dry index confirmed that global trade growth (in volume) should decline again in 4Q19 (bit.ly/36lAa0p), post frontloading in 3Q19.

However, the recent decline was amplified by 2 other ⬇ normalization effects:

1/ Mines run by Vale SA (in #Brazil) resumed production. The sudden ⬆ in shipments in 3Q19 has lifted demand for large ships transporting iron ore and other materials to China.

1/ Mines run by Vale SA (in #Brazil) resumed production. The sudden ⬆ in shipments in 3Q19 has lifted demand for large ships transporting iron ore and other materials to China.

2/ Lower vessel availability explained a part of the bounce in 3Q19 as new scrubbing technology will be used on some ships to meet new emissions restrictions (which took into effect on Jan. 1, 2020).

🇨🇳 #China's heavy #truck sales hit new high in 2019 - Xinhua

*In Dec., around 90,000 heavy trucks were sold, (9% year on YoY), exceeding industrial expectations.

*The sales rose for six consecutive months in the second half.

*Link: bit.ly/2QOu0iH

*In Dec., around 90,000 heavy trucks were sold, (9% year on YoY), exceeding industrial expectations.

*The sales rose for six consecutive months in the second half.

*Link: bit.ly/2QOu0iH

🇩🇪 #Germany new car registrations rise by 19-20% in December - source - Reuters

reuters.com/article/german…

reuters.com/article/german…

🌎 🇰🇷 Samsung Electronics says profit fall likely milder than forecasts as chip prices bottom out - Reuters

reuters.com/article/us-sam…

reuters.com/article/us-sam…

🇨🇳 #CHINA DEC. RETAIL PASSENGER VEHICLE SALES -3.6% Y/Y: PCA - BBG

➡ It's up from -4.2% YoY in Nov. and it was the lowest decline since June 2019.

➡ It's up from -4.2% YoY in Nov. and it was the lowest decline since June 2019.

🌎 #Semiconductors | A revival is under way in the #chip business - The Economist

economist.com/business/2020/…

economist.com/business/2020/…

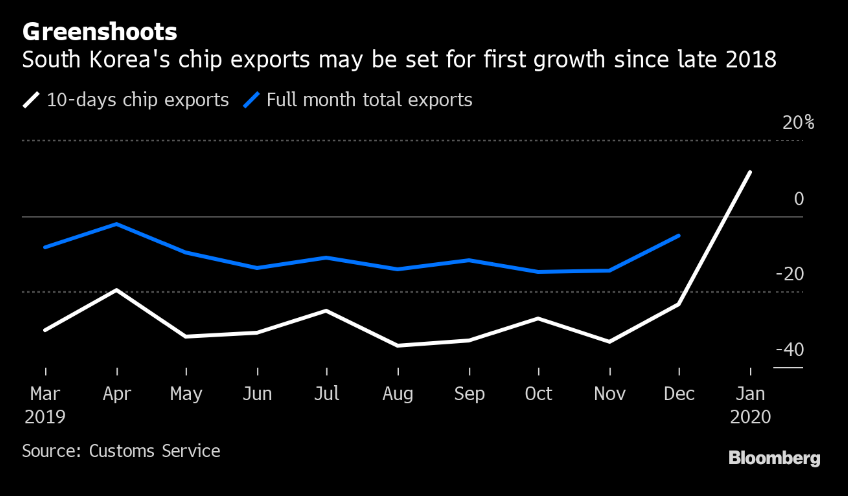

🇰🇷 #SouthKorea Jan 1-10th Exports y/y: +5.3% v +7.7% prior

*Average Daily Exports y/y: +5.3%❗ v +0.5% prior

*#Chip Exports y/y: +11.5%❗ v -23.4% prior (1st ⬆ since Oct. 2018)

*Link (Korean): bit.ly/2TiGqlL

*Average Daily Exports y/y: +5.3%❗ v +0.5% prior

*#Chip Exports y/y: +11.5%❗ v -23.4% prior (1st ⬆ since Oct. 2018)

*Link (Korean): bit.ly/2TiGqlL

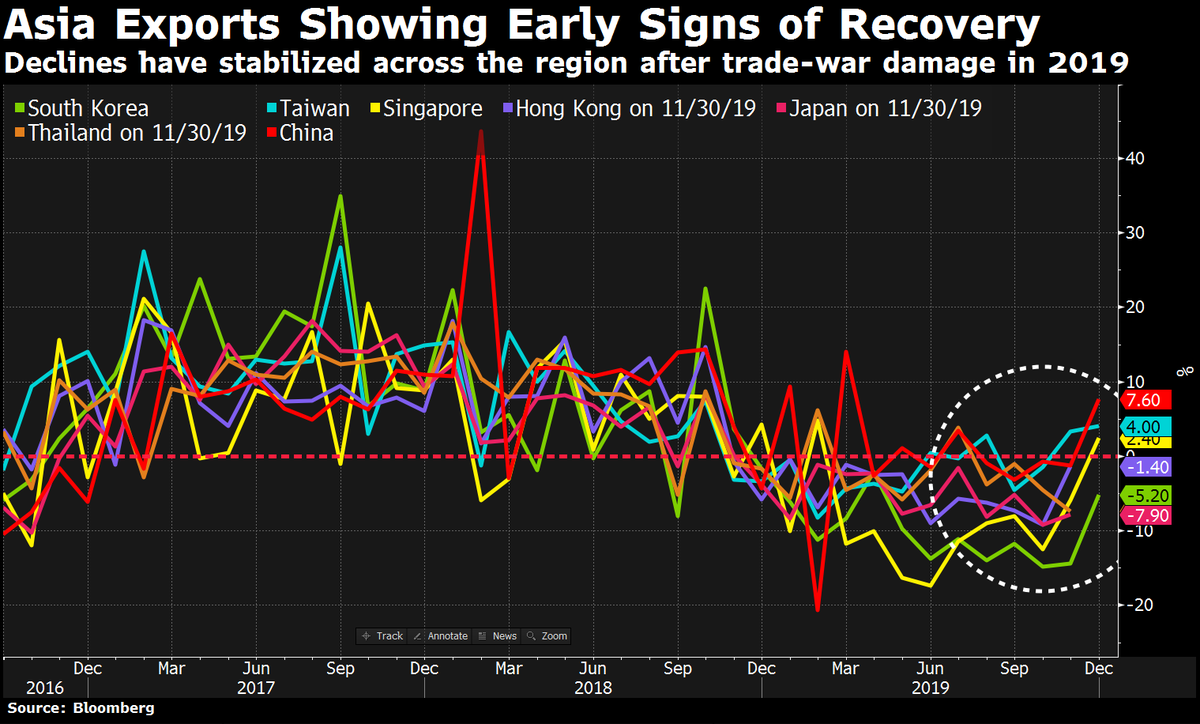

🇨🇳 🌏 #Asia | #China Dec. Exports Y/Y: +7.6% v +2.5%e (largest ⬆ since Mar. 2019)

*#Taiwan Dec. exports ⬆ 4.0% Y/Y (largest ⬆ since Oct. 2018

*#SouthKorea Dec. exports ⬇ 5.2% Y/Y (smallest ⬇ since Apr. 2019)

*Chart from BBG

*#Taiwan Dec. exports ⬆ 4.0% Y/Y (largest ⬆ since Oct. 2018

*#SouthKorea Dec. exports ⬇ 5.2% Y/Y (smallest ⬇ since Apr. 2019)

*Chart from BBG

🌎 #Semiconductors | ASM International reports 4Q orders “slightly above” EU370m, “substantially” surpassing its Oct. 30 view of EU290m-EU310m - Bloomberg

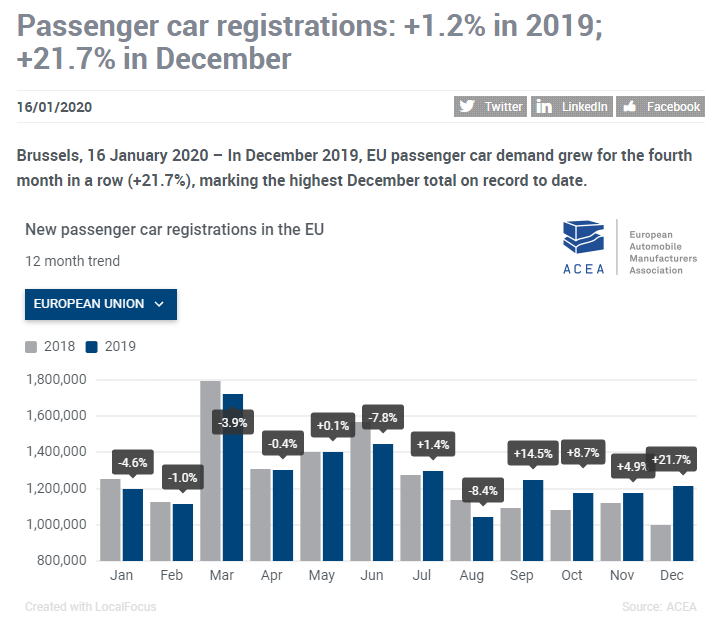

🌎 #Autos | 🇪🇺 In December 2019, EU passenger car demand grew for the fourth month in a row (+21.7% YoY), marking the highest December total on record to date - European Automobile Manufacturers’ Association

*Link: bit.ly/36XwTod

*Link: bit.ly/36XwTod

🇪🇺 🇫🇷 🇳🇱 🇸🇪 Sales also more than doubled in the #Netherlands ahead of an increase to 8% from 4% in the tax rate for electric company cars.

*Bloomberg link: bloom.bg/2uMoqpI

*Bloomberg link: bloom.bg/2uMoqpI

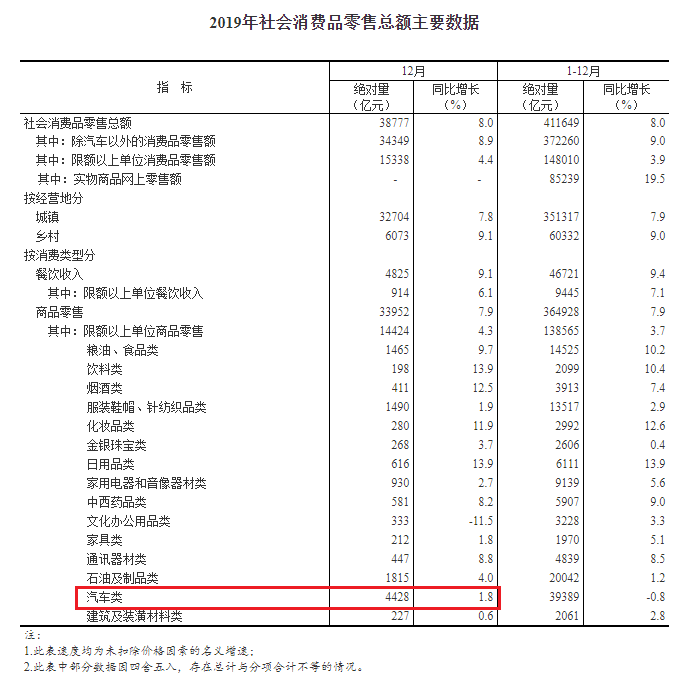

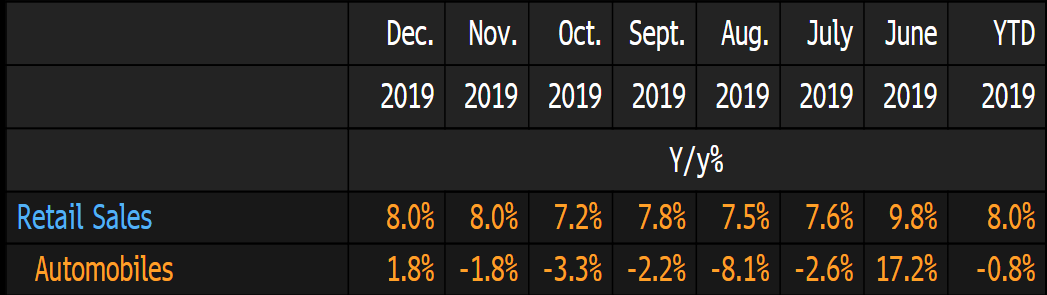

🇨🇳 #China | According to the Retail Sales report, automobiles sales ⬆ 1.8% YoY in Dec. (first positive reading since June 2019).

*Link: bit.ly/36036tX

*Link: bit.ly/36036tX

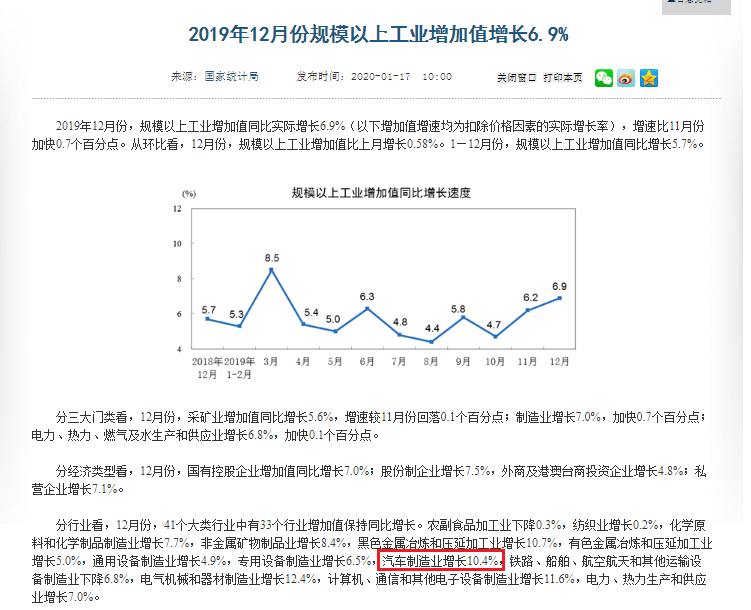

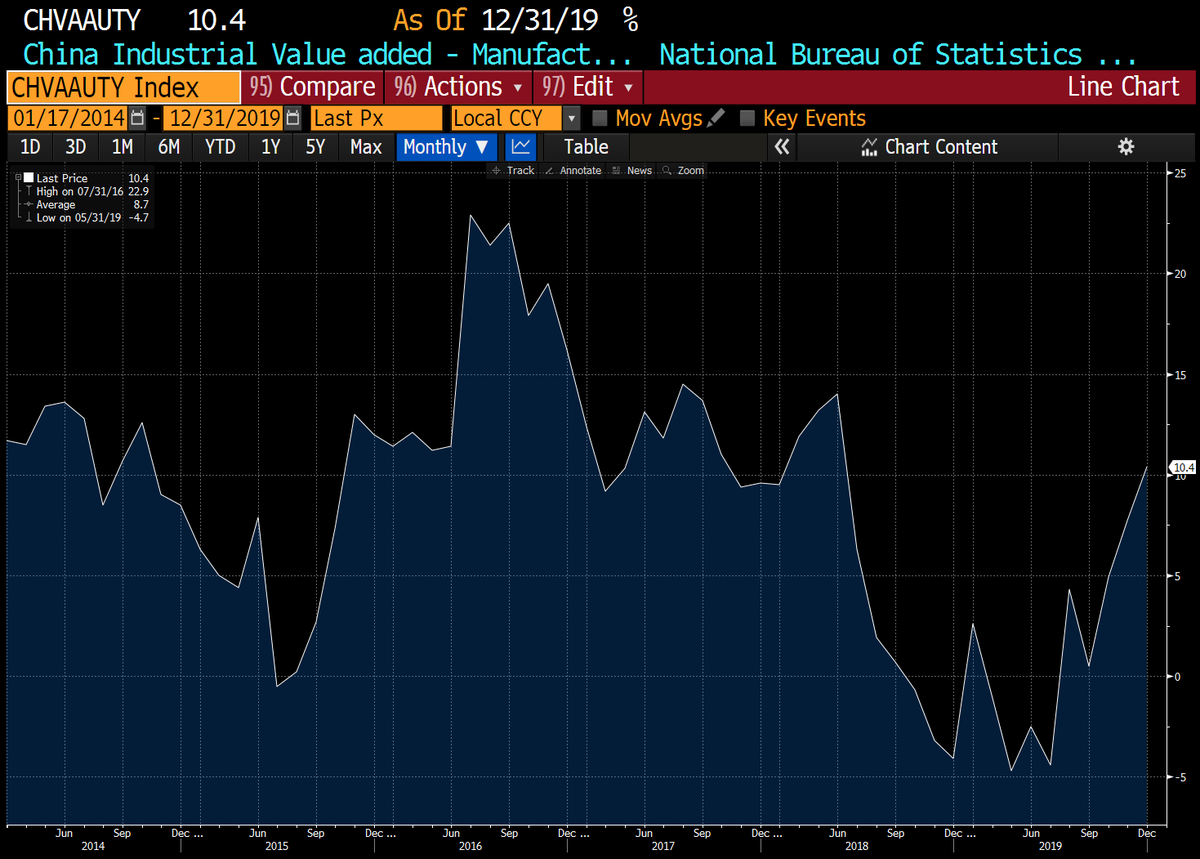

🇨🇳 #China | Dec. #Auto Manufacturing output ⬆ 10.4% YoY (largest ⬆ since June 2018).

*Link (Chinese): bit.ly/2THLRLB

*Link (Chinese): bit.ly/2THLRLB

🇸🇬 #Singapore DEC NON-OIL DOMESTIC EXPORTS Y/Y: +2.4% V -5.9% prior (first ⬆ rise since Feb. 2019)

*It follows positive reading in #Taiwan and #China in Dec. while #SouthKorea also showed a positive print in the first 10 days of Jan (bit.ly/2R3VzWE).

*Chart from BBG

*It follows positive reading in #Taiwan and #China in Dec. while #SouthKorea also showed a positive print in the first 10 days of Jan (bit.ly/2R3VzWE).

*Chart from BBG

🇰🇷 #SouthKorea Jan. 1-20 Exports Y/Y: -0.2% v -2.0% in Dec. 1-20 (highest since Dec. 2018)

*Daily Average Y/Y: -0.2%❗ v -5.1% in Dec. 1-20

*Exports to #China Y/Y: -4.7% v +5.3% in Dec. 1-20

*Link (Korean): bit.ly/3ay6waW

*Daily Average Y/Y: -0.2%❗ v -5.1% in Dec. 1-20

*Exports to #China Y/Y: -4.7% v +5.3% in Dec. 1-20

*Link (Korean): bit.ly/3ay6waW

🇰🇷 #SouthKorea | #Semiconductor Exports Y/Y: +8.7% v -16.7% in Dec. 1-20 (1st increase since Nov. 2018; highest since Oct. 2018)

*Link (Korean): bit.ly/3ay6waW

*Link (Korean): bit.ly/3ay6waW

🌎 #Semiconductors #5G | New Low-Cost iPhone to Enter Mass Production in February - Bloomberg

*Apple expected to launch the 4.7-inch #phone as early as March.

bloomberg.com/news/articles/…

*Apple expected to launch the 4.7-inch #phone as early as March.

bloomberg.com/news/articles/…

🌎 #Semiconductors | #Apple Is Raising #TSMC #Chip Orders to Meet Strong #IPhone Demand - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

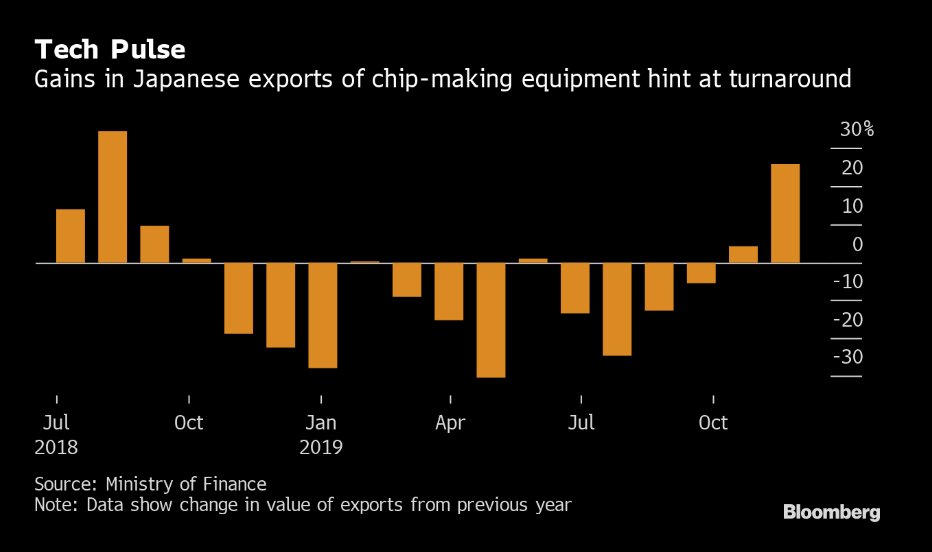

🌎 #Semiconductors | 🇯🇵 #Japan shipments of chip-making equipment rose 25.8% YoY in December (largest increase since Aug. 2018).

*Note: #Chip-manufacturing equipment is a leading indicator of semiconductor demand down the line.

*Link: bit.ly/37neMsi

*Note: #Chip-manufacturing equipment is a leading indicator of semiconductor demand down the line.

*Link: bit.ly/37neMsi

🌎 #Semiconductors | 🇺🇸 Texas Instruments Points to Signs of #Chip Industry Revival - Bloomberg

*TI Statement: prn.to/36hsmvW

bloomberg.com/news/articles/…

*TI Statement: prn.to/36hsmvW

bloomberg.com/news/articles/…

🌎 STMicro earnings beat estimates on demand for next-generation #chips - CNBC

cnbc.com/2020/01/23/reu…

cnbc.com/2020/01/23/reu…

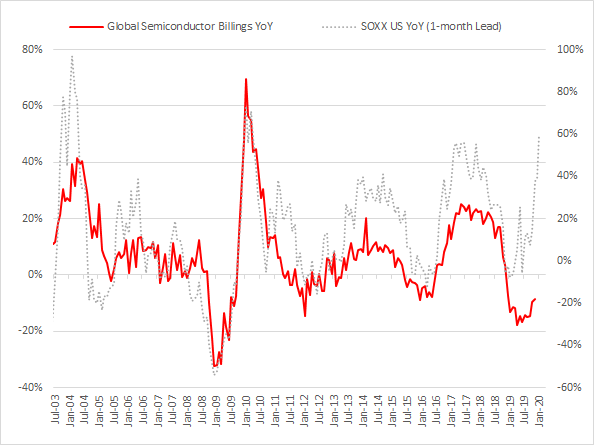

In 2020, global sales of #semiconductors will be supported by a rebound in global shipment of smartphones (bit.ly/2NSMyxJ), servers (bit.ly/30Jly9c), while downward pressures from global #auto sales should ease.

However, the sharp improvement seen very recently could be attributed to transitory factors:

1/ The recent stabilization seen in global auto sales reflected “exceptional” gain in Europe.

1/ The recent stabilization seen in global auto sales reflected “exceptional” gain in Europe.

2/ #Huawei boosted stockpiles supplies ahead of a widely-expected toughening of U.S. #technology sanctions - Nikkei

*#China's biggest telecoms company asks Asian suppliers for up to a year's inventory ❗

asia.nikkei.com/Spotlight/Huaw…

*#China's biggest telecoms company asks Asian suppliers for up to a year's inventory ❗

asia.nikkei.com/Spotlight/Huaw…

In this context, it seems that investors’ expectations are well ahead of the cycle.

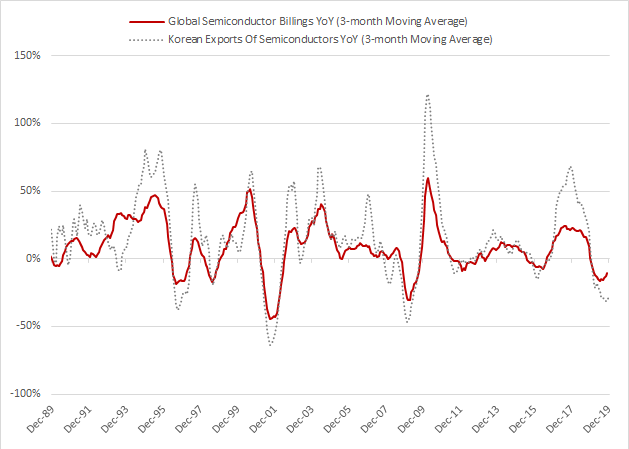

*I updated the previous chart with latest data from WSTS (bit.ly/2RkEgAP) ⬇

*I updated the previous chart with latest data from WSTS (bit.ly/2RkEgAP) ⬇

🇺🇸 🇨🇳 New U.S. Limits on #Huawei Suppliers Coming Soon, Ross Says - Bloomberg

*Link: bloom.bg/3aEEdaI

*Link: bloom.bg/3aEEdaI

🌎 #Semiconductors | Intel Gains as #DataCenter Revival Fuels Revenue Growth - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…